Update from the last post on the Supreme Court decision

There is in fact a huge difference between a tax on people without health insurance and a mandate enforced with a penalty.

A mandate is a mandate, a law that everyone must have health insurance. If the minor penalty envisioned in the ACA isn't sufficient (it's not) to get people to buy health insurance, it was entirely within HHS power to find more effective means of enforcement. They could literally have sent inspectors around and drag you off to jail for not having health insurance.

A tax is only a tax. If you pay the tax, there is nothing else they can do to you. And taxes have to be approved by Congress, not just HHS. And there is no way Congress is going to vote in a $10,000 head tax for not having health insurance.

Since the penalty under the mandate is so much less than the cost of health insurance, it was already pretty clear that they were going to have to start using strong-arm tactics to enforce the mandate.

They could have started by requiring proof of health insurance for getting a passport, student loan or grant, unemployment check, or any other interaction with the Federal Government. That was, according to the fawning New Yorker article on Obamacare, already contemplated. Next, go to the point of sale: they could have required that delivery of any health service must include a check of health-insurance status and report to authorities. They could have used medicare funds to force states to make proof of health insurance a requirement to get a driver's license. In the end, yes, they could have sent inspectors around to check health insurance status and haul people off to jail. You think I'm kidding? They already send inspectors around to check immigration status and haul people off to jail.

Now, none of this can happen. By construing the penalty as a "tax," and holding it unconstitutional as a "mandate," Roberts has clearly said that the penalty is the only recourse the Federal government can use to enforce its mandate. It is only a tax on individuals who don't have health insurance. It is not a law that people must have health insurance, enforceable by the usual array of legal administrative and regulatory sanction.

The minute HHS tries anything beyond the penalty to coerce people to buy health insurance (which it will--it must), HHS will be sued (which it will). The suit will say: "A mandate is unconstitutional. It's only a tax. We paid the tax. Go away." The suit will go to the Supreme Court. In the current court, it will win in a heartbeat.

That pretty much undermines the whole mandate business just as effectively as striking it down would have done.

Saturday, June 30, 2012

The New European Solution

The agreement reached on Thursday in the Eurozone sparked a major stock and bond rally in world financial markets. There was a nearly two percent pop across the globe. The agreement basically made each country responsible for every other country's commercial banking system. The next step will be Eurobonds, which makes every country responsible for the sovereign debt of all the other countries -- "joint and several" is the usual phrase.

Nothing, of course, in the agreement reigns in the growth of that sovereign debt or in way repairs commercial bank balance sheets. There is just a new signatory -- Germany. Now, if one looks only at Germany and ignores the rest of the Eurozone, it is clear that Germany itself is on the road to financial ruin, long before taking on the indebtedness of the likes of Greece, Spain, Italy, etc. The main thing that these agreements do is to eliminate any rational reason for the profligate countries to take any measures to curb their budget deficits or fess up about their commercial banking problems.

In American parlance, Europe has adopted the "extend and pretend" model writ large.

This will, briefly, postpone the day of reckoning -- maybe a week, maybe a month, maybe three months...but not much more than that. Then what: Have the man on the moon guarantee Germany's sovereign debt?

To see a defense of this madness, read Laura d'Andrea Tyson's column in the New York Times this morning. It spells out the usual stuff about how austerity doesn't work, which translates to "let the deficits ride to infinity." Tyson is among those that think that laws that prohibit firing don't really matter much to entrepreneurs. It must be nice to look at this from 30,000 feet in a business class seat and to not face the hard realities that Italian and Spanish business folks face every single day. Maybe on a clear day....

As we have pointed out ad nauseum in this blog, the issue in Europe is one of arithmetic. Sovereign deficits are spiraling off to infinity, while the economies, hampered mainly by over regulation and the welfare state (and not austerity...there is none), are grinding to a halt. Having mother Germany step up to the plate is largely irrelevant to where this all ends. It just means that Germany will suffer the same fate as everyone else.

There is no arguing with numbers. Unless the growing gap between spending and revenues is reversed, which, at present, there are no agreements to do, then sovereign debt in the Eurozone will continue to march toward the sky and bond buyers will continue to run for the exits.

Nothing, of course, in the agreement reigns in the growth of that sovereign debt or in way repairs commercial bank balance sheets. There is just a new signatory -- Germany. Now, if one looks only at Germany and ignores the rest of the Eurozone, it is clear that Germany itself is on the road to financial ruin, long before taking on the indebtedness of the likes of Greece, Spain, Italy, etc. The main thing that these agreements do is to eliminate any rational reason for the profligate countries to take any measures to curb their budget deficits or fess up about their commercial banking problems.

In American parlance, Europe has adopted the "extend and pretend" model writ large.

This will, briefly, postpone the day of reckoning -- maybe a week, maybe a month, maybe three months...but not much more than that. Then what: Have the man on the moon guarantee Germany's sovereign debt?

To see a defense of this madness, read Laura d'Andrea Tyson's column in the New York Times this morning. It spells out the usual stuff about how austerity doesn't work, which translates to "let the deficits ride to infinity." Tyson is among those that think that laws that prohibit firing don't really matter much to entrepreneurs. It must be nice to look at this from 30,000 feet in a business class seat and to not face the hard realities that Italian and Spanish business folks face every single day. Maybe on a clear day....

As we have pointed out ad nauseum in this blog, the issue in Europe is one of arithmetic. Sovereign deficits are spiraling off to infinity, while the economies, hampered mainly by over regulation and the welfare state (and not austerity...there is none), are grinding to a halt. Having mother Germany step up to the plate is largely irrelevant to where this all ends. It just means that Germany will suffer the same fate as everyone else.

There is no arguing with numbers. Unless the growing gap between spending and revenues is reversed, which, at present, there are no agreements to do, then sovereign debt in the Eurozone will continue to march toward the sky and bond buyers will continue to run for the exits.

Friday, June 29, 2012

McDonnell Reappoints Dragas

I like Helen Dragas. I know that may sound strange, but I think she is very smart and well intentioned. We all make mistakes. I think her second term will prove out that she can be an outstanding member of the Board of Visitors.

But, you have to wonder about Governor McDonnell. What's he thinking? He announced the appointment as if the opposition to Dragas was gender based, which is completely ridiculous. What McDonnell still refuses to admit, at least publicly, is that he favored the ouster of Sullivan all along. That is the only conceivable explanation for Dragas's reappointment.

I would not worry about the Board of Visitors ganging up on Sullivan. I don't see that happening. I expect Dragas will be very cooperative and the future is likely to be harmonious.

But, you have to wonder about the Governor in all of this. No matter how you tell the story, the Governor's role is likely not to be one that history will look back on with admiration.

But, you have to wonder about Governor McDonnell. What's he thinking? He announced the appointment as if the opposition to Dragas was gender based, which is completely ridiculous. What McDonnell still refuses to admit, at least publicly, is that he favored the ouster of Sullivan all along. That is the only conceivable explanation for Dragas's reappointment.

I would not worry about the Board of Visitors ganging up on Sullivan. I don't see that happening. I expect Dragas will be very cooperative and the future is likely to be harmonious.

But, you have to wonder about the Governor in all of this. No matter how you tell the story, the Governor's role is likely not to be one that history will look back on with admiration.

Bimbos and Window Dressings.

Do you know her? You should because as per US Govt. she is a “Genius” worthy of special visa for individuals with extra-ordinary ability.

I am not joking. So far her “extraordinary ability” seems to be limited to appearing in the Playboy magazine as their Miss November 2010. Her name is Shera Bechard, the Canadian-born former girlfriend of Playboy Enterprises founder Hugh Hefner. Now you know that America is in trouble.

And if we get time to look around, we may find “Fast and Furious” that I wrote about yesterday is here on schedule. Did someone say that there is no proof of month end window dressing? May be not but there is enough proof of quarter ending window dressing. After the disappoint of no QE 3, it was least they could do to goose up the books, so that the report to the investors would not be that bad. And of course we have to recover the $5 billion that “Whale” lost sometimes back. Or is it $ 9 Billion. What do the small differences matter anyway? It’s all free.

Somehow, we had advance information of these shenanigans and we are not surprised. The 1365 level in the 1st week of July, which I wrote about 15 days back, is almost here. In fact I would love to see it reach 1380 by the end of the week. Because we also know what is next. Don’t be surprised to see that mood has suddenly turned positive and folks start talking about technical indicators giving buy signals. Although you cannot fool all the people all the time, but when Government is on your side, rather when you own the Government, you can come pretty close to that.

So let us enjoy this nice weekend in the grandeur of delusion that we live in free democracy. At least we are lucky enough to buy drinks and gamble as we wish with the food stamps. Isn’t it a great country or what!

Thanks for sharing my take on the end game. Be safe out there.

New Paper

In my "real" academic life, I just finished a new paper, "Continuous-Time Linear Models," find it here if you're curious. It's a pedagogical piece really, showing how to do all the familiar discrete-time time-series tricks in continuous time. Comments welcome. I thought of advertising it as evidence that blogging hasn't turned my mind to mush, but I'm afraid real continuous-time econometricians will see it as proof of the opposite proposition.

The Supreme Court

Conservatives are castigating John Roberts for joining with four liberals to provide a path to constitutionality for Obamacare. Why pick on him? When Republicans are in political control, they do exactly the same thing.

Ever hear of "Americans for Disability Act," "The Prescription Drug Bill," "No Child Left Behind," etc. These are Republican initiatives passed by Republicans. Who were the biggest critics of Sarah Palin after she was the Republican nominee for VP? Karl Rove and Peggy Noonan -- two Republicans. What was her crime? She didn't read the NY Times and thought Russsia was across the Bering Straights (which it is).

Who coined the phrase "voodoo economics" to describe the Reagan tax cut plan? A conservative Republican, that's who. What Governor recently followed the advice of four liberal Democrats, against the advice of conservatives, to try to destabilize the University of Virginia? A conservative Republican that's who.

So, why pick on Roberts? Other than Scott Walker, Mitch Daniels, and Chris Christie, what other Republicans have made any effort at all to roll back the reach of government when they had the chance?

Republicans are only for limiting the reach of government, when they are out of office trying to get in. Once in, they behave like Democrats. So don't pick on Roberts, he's just following tradition. Isn't that what Supreme Court justices are supposed to do?

Ever hear of "Americans for Disability Act," "The Prescription Drug Bill," "No Child Left Behind," etc. These are Republican initiatives passed by Republicans. Who were the biggest critics of Sarah Palin after she was the Republican nominee for VP? Karl Rove and Peggy Noonan -- two Republicans. What was her crime? She didn't read the NY Times and thought Russsia was across the Bering Straights (which it is).

Who coined the phrase "voodoo economics" to describe the Reagan tax cut plan? A conservative Republican, that's who. What Governor recently followed the advice of four liberal Democrats, against the advice of conservatives, to try to destabilize the University of Virginia? A conservative Republican that's who.

So, why pick on Roberts? Other than Scott Walker, Mitch Daniels, and Chris Christie, what other Republicans have made any effort at all to roll back the reach of government when they had the chance?

Republicans are only for limiting the reach of government, when they are out of office trying to get in. Once in, they behave like Democrats. So don't pick on Roberts, he's just following tradition. Isn't that what Supreme Court justices are supposed to do?

Germany Slowly Getting Pulled In

What was a disastrous future for the southern periphery of Europe is now being extended to the northern states as well. Germany is the main target of this exercise. Today's agreement to accept near worthless bank equity by the European banking stabilization fund is an admission of hopelessness.

No one yet is reducing the yawning deficits or recapitalizing the insolvent banks that plague Europe. That's off the table for now. So, European debt continues to explode off to infinity while the paper-shuffling politicians rearrange the names of the guarantors. In the end, it won't matter. Germany will suffer the same fate as Greece and for the same reason. They can't pay their bills.

The problem in Europe is one of solvency, not one of liquidity. These patch jobs only make the final outcome much more severe than it would be if the real problems were faced with candor.

No one yet is reducing the yawning deficits or recapitalizing the insolvent banks that plague Europe. That's off the table for now. So, European debt continues to explode off to infinity while the paper-shuffling politicians rearrange the names of the guarantors. In the end, it won't matter. Germany will suffer the same fate as Greece and for the same reason. They can't pay their bills.

The problem in Europe is one of solvency, not one of liquidity. These patch jobs only make the final outcome much more severe than it would be if the real problems were faced with candor.

Thursday, June 28, 2012

Patriotic Rally?

All the noise for less than three points? Definitely not worth it. If you jumped on the short side during the day, you must be very disappointed today. May be one more attempt to the downside will be made tomorrow. But so far 1300 level have held throughout the week and depending up what happens tomorrow, I think we have a tradable base for the next patriotic rally. I better give a nice name to the coming rip. How about “Fast and Furious”? Congress and Holders both should be happy.

What caused today’s massive “U” turn, only the manipulators know. Rumour is, someone purchased $ 3 billion worth of emini contracts and that caused the stampede. Whatever it is, it is not a definite trend. Just stupid gyration of momentum chasing bots. And while we will get another rip soon, selling is by no means over. I keep writing, there is no panic in the market and as such no bottom yet. May be the bottom will come around 1230 or so and it will come by end of July.

Whatever it is, this guy cannot stop smiling today. Although the Court said the Obamacare is a tax on American people but the congress has constitutional right to tax Americans. It was a funny kind of day when FIX news and largely irrelevant CNN came out shouting that Obamacare has been repelled by US Supreme Court and then the stock market revert back up on some other rumour. But Gold and crude did not recover much. Crude is over sold by a mile and is due for a bounce. May be it will bounce along with the equities next week.

The real news was that Barclays Bank has been caught with its hand in the cookie jar. The fine it has been asked to pay, $ 450 million + is just a slap on the wrist and is nothing compared to the tsunami of legal challenges facing it. I think it will have to make provisions for billions of dollars of legal settlements. Who might be the losers in this rigging? One group that comes to mind are the investors who purchased short term bonds from the banks linked to LIBOR rate. The name of the guy looking over it is Bob Diamond. Kind of rimes with Dimon, whose bank now appears to be sitting over a loss of over $ 5 billion. And when they are caught red handed in wrong doing, they blame the small fishes in the food chain. The boss gives tacit approval for the wrong and illegal acts and collects millions of dollars of bonuses. Just what Barclays did between 2005 and 2009. And it is not just Barclays, HSBC, RBC, CITI, UBS and many others are involved. Is it any wonder that the Bankers are vilified and called Banksters? There is “Systemic Dishonesty” in everything that these TBTF Banks do. But nothing will happen to the big bosses. Didn’t we just see that during the Senate hearing of Jamie Dimon?

Tomorrow there will be photo-ops from the Euro leaders and some sort of statement. While for the sake of market, I think they say something soothing, personally I hope Germany tells them all to drop dead. Now the Euro cup final will be played between Spain and Italy. This is what is called “Battle of two losers”. ECB must be very proud that both its sponsored countries have made it to final.

Anyway, the last day of June is mostly bearish. Dow down 15 of the last 20 and Nasdaq down 6 straight. I think it will be down day tomorrow and that fits well with the pattern of 2011. Last July there were 5 red days before it made the final top. So far we have 4 red days. So one more red day is in order. Tomorrow will tell the story.

That’s it for today. Thanks for reading http://bbfinance.blogspot.com/ . Please join me in Twitter (@BBFinanceblog) and do re-tweet the post if you agree with it.

My 2 Cents on the Supreme Court and Obamacare

I think the court did the right thing. And pretty much what I expected.

They overturned the mandate under the commerce clause. Hoorray! There is some limit to the commerce clause! I think they had to do this. If they upheld the whole thing, they would have said there is no limit whatsoever to Federal power.

They upheld the mandate as a tax. Swallow hard, free-market friends.

If the Federal government has the power to adjust your taxes based on whether you buy an electric car, cover your roof with solar panels, use 1 btu of petroleum to create 1 btu of corn ethanol, take out a mortgage on your mansion, hire a nanny to take care of your kids, and all the other silly things it does in the tax code, it surely has the power to adjust your taxes based on whether you buy health insurance.

Roberts: "The Constitution permits such a tax, it is not our role to forbid it, or to pass upon its wisdom or fairness."

Yes, the administration didn't call it a tax. But for the court to overturn this whole law, one of the Administration's proudest accomplishments, based on that technicality would have been petty and political. They did the right thing to look at the big picture.

I think our country needs a lot more Supreme Court decisions that say "we think this is a really stupid policy, but alas, it is constitutional." (And, "we think this is a great policy, but alas it oversteps the constitution.")

As I said before, the mandate was never the weakest part of this law as a matter of economics. It's the rest of the perfectly constitutional thousands of pages, and the perfectly constitutional thousands more arbitrary regulatory decisions that are the problem. Relying on the court to throw out the bathwater on the basis of the mandate was always a stretch.

We should not rely on the court to determine economic policy or write laws. That's what Congress and Administration are for. If you don't like the health care law, try to find someone of either party with the courage to say just how he or she will repeal and replace, and vote.

This will be healthy for both parties. Defenders can't say how wonderful it would all have been except that the nasty polticized court threw it out. They will have to own Obamacare as it falls apart at the seams. Opponents will have to work to repeal, and explain what they will replace with.

Yes, it would be nice if the constitution forbade silly economic policy, and it would be nice if it forbade arbitrary discretionary regulation. For that you need to overturn a century's worth of precedents. Nobody even asked the court to do that in this case. (Time to start!)

Disclaimer: This is based just on news reports. I haven't read the decision yet, and will comment more when I do. There are lots of other issues.

Update: Two more cents here in a follow-up post. "Tax" and "Mandate" really are very different in important ways.

They overturned the mandate under the commerce clause. Hoorray! There is some limit to the commerce clause! I think they had to do this. If they upheld the whole thing, they would have said there is no limit whatsoever to Federal power.

They upheld the mandate as a tax. Swallow hard, free-market friends.

If the Federal government has the power to adjust your taxes based on whether you buy an electric car, cover your roof with solar panels, use 1 btu of petroleum to create 1 btu of corn ethanol, take out a mortgage on your mansion, hire a nanny to take care of your kids, and all the other silly things it does in the tax code, it surely has the power to adjust your taxes based on whether you buy health insurance.

Roberts: "The Constitution permits such a tax, it is not our role to forbid it, or to pass upon its wisdom or fairness."

Yes, the administration didn't call it a tax. But for the court to overturn this whole law, one of the Administration's proudest accomplishments, based on that technicality would have been petty and political. They did the right thing to look at the big picture.

I think our country needs a lot more Supreme Court decisions that say "we think this is a really stupid policy, but alas, it is constitutional." (And, "we think this is a great policy, but alas it oversteps the constitution.")

As I said before, the mandate was never the weakest part of this law as a matter of economics. It's the rest of the perfectly constitutional thousands of pages, and the perfectly constitutional thousands more arbitrary regulatory decisions that are the problem. Relying on the court to throw out the bathwater on the basis of the mandate was always a stretch.

We should not rely on the court to determine economic policy or write laws. That's what Congress and Administration are for. If you don't like the health care law, try to find someone of either party with the courage to say just how he or she will repeal and replace, and vote.

This will be healthy for both parties. Defenders can't say how wonderful it would all have been except that the nasty polticized court threw it out. They will have to own Obamacare as it falls apart at the seams. Opponents will have to work to repeal, and explain what they will replace with.

Yes, it would be nice if the constitution forbade silly economic policy, and it would be nice if it forbade arbitrary discretionary regulation. For that you need to overturn a century's worth of precedents. Nobody even asked the court to do that in this case. (Time to start!)

Disclaimer: This is based just on news reports. I haven't read the decision yet, and will comment more when I do. There are lots of other issues.

Update: Two more cents here in a follow-up post. "Tax" and "Mandate" really are very different in important ways.

Wednesday, June 27, 2012

In No Man's Land.

We are in that zone again, that 30 point up or down move day after day from middle of May onward.

By and large there is not much action really in the market and it is as if folks are going though the motion for the benefit of day traders. Or is this the calm before the storm? And already the hourly charts have moved from over- sold to over- bought.

Today everything was up. Equities, gold, crude, bond and US $. The divergence between equities and FX is quite big.

So who will catch up? If there is some good news from the four wise leaders of Europe, may be Euro will go up and equities will reach moon. We will have to wait and see. If on the other hand, nothing comes out of the 913th Euro meeting, we may see bit of selling. Tomorrow is going to another important (impotent?) day for the market. The fate of Obamacare will be decided and then news from Euro summit. As you all know, I hate to take or even suggest to take any position before uncertainty.

I am still debating whether to take any long position in the coming rip-fest. It will be like what I wrote yesterday: picking up pennies in front of a steam roller. There is nothing in the market except central bank liquidity which can move the market higher. Either the Fed or ECB or someone from somewhere will have to feed the junkies. Till that happens, the road is pointing down.

I think the best trade now would be to wait for the market to reach either resistance or support and see if they hold. It is not necessary to force a trade here or take a trade just because we are bored. In the mean time,let me share with you a nugget of gold, an Analog which is not silly.

(Hat Tip: ED Matts)

Thanks for reading http://bbfinance.blogspot.com/. Please do re-tweet if you think it is useful.

Mostly Winners -- Two Losers

Now that the UVA crisis has passed it is easy to see that the ultimate outcome created winning positions for mostly everyone involved. Even Rector Helen Dragas emerged with strength and character in bowing to the inevitable return of President Teresa Sullivan. It is unfortunate that Mark Kington and Peter Kiernan remain on the outside looking in. Both Kington and Kiernan are outstanding alums and their contributions to the University in the past merit returning these two to positions of respect at their alma mater. I for one hope to see both Kington and Kiernan playing a major role at the University in the years ahead, as they have in the past.

There are a lot of messages in what has transpired in the past two weeks, but reflect for a moment on why the groundswell of support for Sullivan was so overwhelming. Sullivan did the little things well. She was kind and friendly. She sought out all parts of the University community. She expressed interest in everything that we do. These things count. It was difficult to see her ouster as warranted and to see the process as fair. Underneath it all, the personality and humility of Terry Sullivan were her best weapons. She disarmed the community and her opponents with her affable style.

One major loser was the Governor. He did nothing to stop this process and more than one insider openly mentioned the Governor as a major mover in the effort to unseat Sullivan. Insiders are well aware of the Governor's true, as opposed to stated, role in all of this and, in due time, the public will know as well.

Another major loser was the Wall Street Journal, whose editorial "Virginia Fracas" contains more inaccuracies per paragraph than anything I've ever read. Moreover, the overriding theme of the editorial is totally inaccurate -- that this was a battle between reform and anti-reform. Nothing could be further from the truth. Today's WSJ article is similarly misleading for readers unencumbered with the facts. The WSJ has embarrassed itself with its coverage of the Sullivan crisis and makes one wonder about its coverage of other issues.

Hopefully true reform, as opposed to rearranging deck chairs, can come to the University now that this drama has ended.

There are a lot of messages in what has transpired in the past two weeks, but reflect for a moment on why the groundswell of support for Sullivan was so overwhelming. Sullivan did the little things well. She was kind and friendly. She sought out all parts of the University community. She expressed interest in everything that we do. These things count. It was difficult to see her ouster as warranted and to see the process as fair. Underneath it all, the personality and humility of Terry Sullivan were her best weapons. She disarmed the community and her opponents with her affable style.

One major loser was the Governor. He did nothing to stop this process and more than one insider openly mentioned the Governor as a major mover in the effort to unseat Sullivan. Insiders are well aware of the Governor's true, as opposed to stated, role in all of this and, in due time, the public will know as well.

Another major loser was the Wall Street Journal, whose editorial "Virginia Fracas" contains more inaccuracies per paragraph than anything I've ever read. Moreover, the overriding theme of the editorial is totally inaccurate -- that this was a battle between reform and anti-reform. Nothing could be further from the truth. Today's WSJ article is similarly misleading for readers unencumbered with the facts. The WSJ has embarrassed itself with its coverage of the Sullivan crisis and makes one wonder about its coverage of other issues.

Hopefully true reform, as opposed to rearranging deck chairs, can come to the University now that this drama has ended.

Tuesday, June 26, 2012

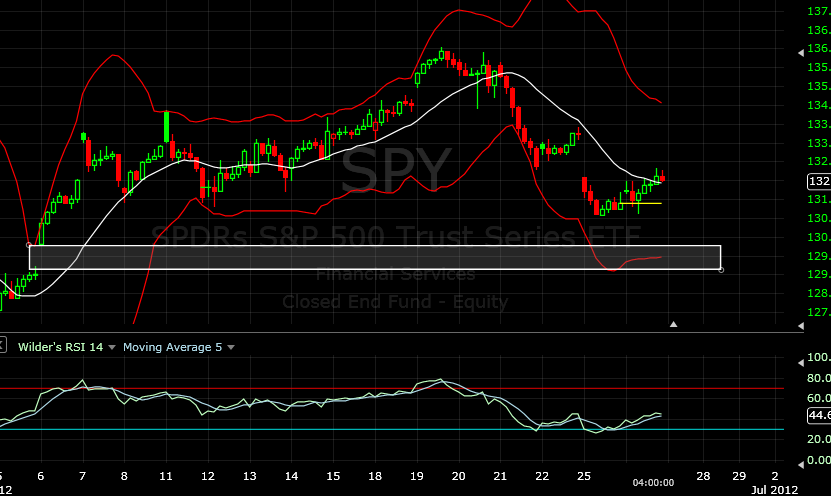

Bear Flag and Unfilled Gap.

I am not an expert in TA, not by a long shot. More of an arm chair technical analyst. But it looks like a bear flag to me. What do you think?

Also there is this area of unfilled gap which I have been writing about for a while and that is my target area before any bounce. Well, if the market decides to ignore that gap, I cannot argue with it but I think chances are high that tomorrow we will see another down day and maybe we will get a chance to fill that gap. That is also the area of strong support. All in all, not yet right time to play for the bounce.

If you look at the chart of yesterday, we were due for this green day. Should I call this an Analog? Nah! I don’t have much faith on Analogs. They are fun to watch when they happen, but it is suicidal to take action based on Analogs. We better have some other edge in trading or investing.

Nothing changed fundamentally in the world today. Despite the tension in Middle East, Crude did not budge much. Gold is hanging there by a thread. Euro land remained front and centre of the market. And no one is talking about the bigger mess that is America. But this constant up and down without a clear direction is draining for both the bulls and bears. You really have to be super smart to win in this market or luck or both. The last sell-off which took SPX from 1358 to 1314 has severely discouraged the bulls. Today it gained a mere 6 points which it may give back tomorrow and some more. If the plan is to discourage retail and then jack up the whole thing on super light volume, then it is successful. We will soon know. Even if we want to play for a bounce, it has to be super quick and for a very short time.

Every world leader is talking of growth and austerity. The leaders of the failed states like Greece or Spain are blaming Austerity for the ills of their country. But where is this “Austerity” that they keep talking about? They have not reduced spending. Per latest report, Greece did not reduce the number of its public sector employees that it agreed when it took the bailout. Why I am not surprised. What austerity measures Spain took or for that matter France or Britain? What % of GDP they saved through Austerity? What these countries have been doing all these years if they are talking about Growth only now? Politicians are same everywhere be it Spain or Uganda. May be now-a-days they are less corrupt in Uganda.

But these things will run its own course and nothing will change however we may shout. We just want to eke out a living and survive from these crooks. That’s it for today. Thanks for reading http://bbfinance.blogspot.com/ . Please do re-tweet of you think it is useful.

Harmony at UVA

The UVA Board of Visitors voted today 15-0 to return Teresa Sullivan to her post as President of the University. In a gesture of unity, the Board conducted a 15-0 vote of confidence for the Rector, Helen Dragas. Truly!

These are welcome actions and hopefully now the University can address the real issues that seemed to divide the President and the Board that, heretofore, had never surfaced at a Board meeting. It is time to talk about these things in the open and begin a much needed move to reform an ossified, bureaucratic institution, that is in much need of reform.

UVA, like other major American Universities, faces an uncertain future because, while costs have gone through the roof, the quality of education provided has stagnated. It is time to face these problems squarely and not pretend that all is well in academia. All is not well.

The UVA Board has corrected an egregious error and should be commended. Removing a sitting President, without so much as a meeting or a vote or even a discussion at a board meeting, could never provide the Sullivan removal with even a bare minimum figleaf of legitimacy.

Board member Hunter Craig was the real hero, fighting tirelessly to get the votes necessary to call a meeting to reconsider and then to follow up and ultimately create the conditions that would lead to a unanimous board vote to return Sullivan to her post. Together with Heywood Fralin, Craig's leadership has rescued UVA from the brink.

All in all...a good day for UVA!

These are welcome actions and hopefully now the University can address the real issues that seemed to divide the President and the Board that, heretofore, had never surfaced at a Board meeting. It is time to talk about these things in the open and begin a much needed move to reform an ossified, bureaucratic institution, that is in much need of reform.

UVA, like other major American Universities, faces an uncertain future because, while costs have gone through the roof, the quality of education provided has stagnated. It is time to face these problems squarely and not pretend that all is well in academia. All is not well.

The UVA Board has corrected an egregious error and should be commended. Removing a sitting President, without so much as a meeting or a vote or even a discussion at a board meeting, could never provide the Sullivan removal with even a bare minimum figleaf of legitimacy.

Board member Hunter Craig was the real hero, fighting tirelessly to get the votes necessary to call a meeting to reconsider and then to follow up and ultimately create the conditions that would lead to a unanimous board vote to return Sullivan to her post. Together with Heywood Fralin, Craig's leadership has rescued UVA from the brink.

All in all...a good day for UVA!

Sand in the gears

Today's Wall Street Journal has a beautifully informative editorial, "Employment, Italian Style." Snippets:

The journal writes,

Labor tax wedges of 40-50%, to which we must add “non-tax compulsory payments (NTCPs)” which "represent a strong increase over and above the overall tax burden. E.g., in 2011, the compulsory payment wedge for the average single worker was 50.4% compared with the corresponding tax wedge of 47.6%" And remember, once they give you a euro, you still pay another 21% VAT before you can eat that plate of delicious pasta. But the WSJ paragraph suggests 47.6% is the effective wedge of regulation on top of explicit taxation. (If readers know where it came from, add a comment.)

Also left out is the effect of this kind of hyper-regulation on corruption. You can imagine when the inspector comes in to see if all the paperwork is up to date how the conversation evolves. (Ask Luigi Zingales)

Cleaning up this mess is what we mean by "structural reform." How to achieve it politically seems like a nightmare to me. Fighting each of ten thousand regulations one by one seems hopeless. Each one sounds good, each one taken alone seems minor, each one has an entrenched interest backing it and an army of bureaucrats whose jobs depend on its enforcement. And the economy dies the death of a thousand cuts. Can you really abolish it all in one fell swoop or grand bargain?

Certainly not if you don't try.

The WSJ headline was

Once you hire employee 11, you must submit an annual self-assessment to the national authorities outlining every possible health and safety hazard to which your employees might be subject. These include stress that is work-related or caused by age, gender and racial differences. You must also note all precautionary and individual measures to prevent risks, procedures to carry them out, the names of employees in charge of safety, as well as the physician whose presence is required for the assessment.This kind of thing is hard to track down. You can't easily find a prepackaged "list of regulatory sand in the gears lowering productivity and employment in Italy," the way we can find (statutory) tax rates, spending numbers, interest rates, and so on. So like the drunk in the old joke, looking for his car keys under the light even though he knows he dropped them a block a way, much economic discussion focuses on those headline issues ("Stimulus!" "Austerity!" "Bailout!" "Leave the Euro!" "Raise/lower taxes!") and ignores all the sand in the gears.

Once you hire your 16th employee, national unions can set up shop. As your company grows, so does the number of required employee representatives, each of whom is entitled to eight hours of paid leave monthly to fulfill union or works-council duties. Management must consult these worker reps on everything from gender equality to the introduction of new technology

Hire No. 16 also means that your next recruit must qualify as disabled. By the time your firm hires its 51st worker, 7% of the payroll must be handicapped in some way,...

Once you hire your 101st employee, you must submit a report every two years on the gender dynamics within the company. This must include a tabulation of the men and women employed in each production unit, their functions and level within the company, details of compensation and benefits, and dates and reasons for recruitments, promotions and transfers, as well as the estimated revenue impact....

The journal writes,

All of these protections and assurances, along with the bureaucracies that oversee them, subtract 47.6% from the average Italian wage, according to the OECD.I wish the WSJ had footnotes or links, even in its online edition, to make it easier to track down numbers of this sort. A quick tour through the OECD website provides some horrifying numbers on

Labor tax wedges of 40-50%, to which we must add “non-tax compulsory payments (NTCPs)” which "represent a strong increase over and above the overall tax burden. E.g., in 2011, the compulsory payment wedge for the average single worker was 50.4% compared with the corresponding tax wedge of 47.6%" And remember, once they give you a euro, you still pay another 21% VAT before you can eat that plate of delicious pasta. But the WSJ paragraph suggests 47.6% is the effective wedge of regulation on top of explicit taxation. (If readers know where it came from, add a comment.)

Also left out is the effect of this kind of hyper-regulation on corruption. You can imagine when the inspector comes in to see if all the paperwork is up to date how the conversation evolves. (Ask Luigi Zingales)

Cleaning up this mess is what we mean by "structural reform." How to achieve it politically seems like a nightmare to me. Fighting each of ten thousand regulations one by one seems hopeless. Each one sounds good, each one taken alone seems minor, each one has an entrenched interest backing it and an army of bureaucrats whose jobs depend on its enforcement. And the economy dies the death of a thousand cuts. Can you really abolish it all in one fell swoop or grand bargain?

Certainly not if you don't try.

The WSJ headline was

Prime Minister Mario Monti has issued a new "growth decree" to revive Italy's moribund economy. Among other initiatives, the 185-page plan proposes discount loans for corporate R&D, tax credits for businesses that hire employees with advanced degrees,..Not to belabor the obvious, but this is incredibly depressing. More special programs are not what Italy needs. I hope there are better ideas in the rest of the 185 pages.

Strangled by Regulation

The American economy isn't going anywhere. Even a Supreme Court decision against the Obamacare mandate can't fix the absence of commercial and residential lending mandated by Dodd-Frank. American business is strangling under the heavy boot of government. Hiring is simply irrational given the political and regulatory environment.

The energy industry will do well and there will be technology shows of strength, but the broader economy is weighted down by regulatory red tape and bureaucratic mistrust of free enterprise. All of this bodes ill for the prospects of those seeking employment. All the rhetoric about inequality and taxing the rich simply reinforce all of the reasons why business has no interest in adding jobs.

Unless and until the political environment changes in the direction of free enterprise, the American economy will remain on its present course, sputtering along with no real sense of direction.

The energy industry will do well and there will be technology shows of strength, but the broader economy is weighted down by regulatory red tape and bureaucratic mistrust of free enterprise. All of this bodes ill for the prospects of those seeking employment. All the rhetoric about inequality and taxing the rich simply reinforce all of the reasons why business has no interest in adding jobs.

Unless and until the political environment changes in the direction of free enterprise, the American economy will remain on its present course, sputtering along with no real sense of direction.

A Learning Process

Normally, each morning I can't wait to read the Wall Street Journal's opinion pieces, hoping to learn more about news events that may not be captured in the regular news sources. Or, to get a point of view that you rarely see in mainstream media. This morning, I simply passed it by.

Somehow after the lies and misrepresentations in yesterday's WSJ editorial entitled "Virginia Fracas," I don't trust the WSJ any more. Virtually, every paragraph of the "VF" article was an apparently deliberate attempt to distort what is really happening at UVA to fit a narrow political agenda. Shame on WSJ. I doubt that I will have any interest in perusing the WSJ editorial page in the future. I simply don't think the WSJ can be trusted to be truthful when they have a political point to make.

You live and learn.

Somehow after the lies and misrepresentations in yesterday's WSJ editorial entitled "Virginia Fracas," I don't trust the WSJ any more. Virtually, every paragraph of the "VF" article was an apparently deliberate attempt to distort what is really happening at UVA to fit a narrow political agenda. Shame on WSJ. I doubt that I will have any interest in perusing the WSJ editorial page in the future. I simply don't think the WSJ can be trusted to be truthful when they have a political point to make.

You live and learn.

Monday, June 25, 2012

Calvin Economics.

So far things are going as anticipated. No major surprise yet. The 1300 line held in SPX and the gap in SPY has not yet been tested. It is as if the last 15 trading seasons did not happen. Why last 15, we are back to where we were on January 31st of this year. All the euphoria of March now seems like a distant dream. The moods are as gloomy as it can get and yet folks are so conditioned with the Bernanke tonic that there is no real fear or panic in the market. Here in North America, we have found a good scapegoat to blame, that is Europe and particularly Germany. Why Germany is refusing to wallow in the mud like the rest of the PIIGS? Why it is refusing to do the same thing that others have done, i.e. borrow and spend what they do not have. Yes, the poor Greeks may have lied and cheated and extorted and spent money which was not their in the first place but so what. After all, you can print money out of thin air. Hasn’t the great super power America done that over and over again? Nothing has happened to America, yet. But do not despair, even if Germany is not ready to walk to path of destruction, the great nation of American is committed to kick the can down the road. Till the road ends. And all roads end somewhere sometime. But I do not know much. To understand it better, ask Calvin how it works.

Enough of macro economic nonsense. There are smarter people than me, like Bernanke or Kurgman, who know what is best for America. I am just concerned how I do save what little I have from these gentlemen and their brothers. This weakness / sell-off in market was well anticipated and I wrote that there will one more bounce in the 1st week of July. In the very short term, the question is, when does that bounce starts and when does it end. I think it is possible that we will see little more selling. Then on Thursday the honorable manipulators will have something to hang their coats on from Europe. The last two days of window dressing can start in earnest whereby they can suck in the fresh 401K money coming in the market in the beginning of July. So I would expect bounce from Wednesday or Thursday till about the 1stweek of July. Do we play this bounce? It all depends. Are we investors? If so, stay away. Are we nimble traders? Then give it a shot. But remember, it is like picking up pennies in front of a turbo charged steam roller and the steam roller has aids. (Hat tip: Josh Brown). Short term, one hour charts are bit oversold and a bounce can happen.

The pattern is looking so similar to last year.

No need to match 2011 SPX with 2012 AUD and then match 2012 AUD with 2012 SPX. If you like analogs, simply match 2011 SPX with 2012 SPX. Such a rally is a selling opportunity but be aware of the levels.

I think July will be very exciting for the bears. Because unless there is pain and panic, Bernanke will not be able to hand out money. I am repeating myself 461 times now but so far my theory has proved right. There is only so much wiggle room left for these bright folks. It is like playing chess and anticipating the next move of your opponent. Only we are playing against those who want to fool us forever. With its ZRIP policy, the Fed is forcing Pension funds and ordinary investors to take unnecessary risk while on the other hand it provides free money to the TBTF banks to bet against. With no growth in income, job or economy, you can easily guess the direction of the market, no need for a PHD.

Thanks for reading http://bbfinance.blogspot.com/. Please forward / re-tweet / post it on your wall and join me in twitter. (Twitter @ BBFinanceblog)

McCloskey Wisdom

I recommend a gorgeous essay by Deirdre McCloskey, "Factual Free Market Fairness" (hat tip, Kyle N's comment on Sunday's post "Legal News"). Some choice bits:

The case for free markets, and social freedom, is practical. It need not be ideological. It's based on the clear lessons of history. We all have the same stated goals. It's not about who cares more. It's about what works.

Admire McCloskey's post also for the writing. The author of "The Rhetoric of Economics" (Article and Book -- an absolute must-read for every young economist) knows what she's doing! Rather than write an article expanding on one of these points, or a three-volume encyclopedia explaining the factual basis of all of them, she make the withering case by stating each point just once, but layering all of them in one place.

I’m from economics and history, and I’m here to help you... The High-Liberal political philosophers... rely...on a factual story which they take to be so obvious as to not require defense. I claim that on the contrary their master narrative is mistaken, as anthropology or economics or history.

The story is, in a few brief mottos to stand for a rich intellectual tradition since the 1880s: Modern life is complicated, and so we need government to regulate. Government can do so well, and will not be regularly corrupted. Since markets fail very frequently the government should step in to fix them. Without a big government we cannot do certain noble things (Hoover Dam, the Interstates, NASA). Antitrust works. Businesses will exploit workers if government regulation and union contracts do not intervene. Unions got us the 40-hour week. Poor people are better off chiefly because of big government and unions. The USA was never laissez faire. Internal improvements were a good idea, and governmental from the start. Profit is not a good guide. Consumers are usually misled. Advertising is bad. ....It goes on like this. There's no need for me to keep quoting. Just go bask in the whole original.

No. The master narrative of High Liberalism is mistaken factually. Externalities do not imply that a government can do better. Publicity does better than inspectors in restraining the alleged desire of businesspeople to poison their customers. Efficiency is not the chief merit of a market economy: innovation is. Rules arose in merchant courts and Quaker fixed prices long before governments started enforcing them.

How do I know that my narrative is better than yours? The experiments of the 20th century told me so. ...anyone who after the 20th century still thinks that thoroughgoing socialism, nationalism, imperialism, mobilization, central planning, regulation, zoning, price controls, tax policy, labor unions, business cartels, government spending, intrusive policing, adventurism in foreign policy, faith in entangling religion and politics, or most of the other thoroughgoing 19th-century proposals for governmental action are still neat, harmless ideas for improving our lives is not paying attention.

In the 19th and 20th centuries ordinary Europeans were hurt, not helped, by their colonial empires. Economic growth in Russia was slowed, not accelerated, by Soviet central planning. American Progressive regulation and its European anticipations protected monopolies of transportation like railways and protected monopolies of retailing like High-Street shops and protected monopolies of professional services like medicine, not the consumers. “Protective” legislation in the United States and “family-wage” legislation in Europe subordinated women. State-armed psychiatrists in America jailed homosexuals, and in Russia jailed democrats. Some of the New Deal prevented rather than aided America’s recovery from the Great Depression.

Unions raised wages for plumbers and auto workers but reduced wages for the non-unionized. Minimum wages protected union jobs but made the poor unemployable. [JC: In both cases, I would add, minorities were especially hurt.] Building codes sometimes kept buildings from falling or burning down but always gave steady work to well-connected carpenters and electricians and made housing more expensive for the poor. Zoning and planning permission has protected rich landlords rather than helping the poor. Rent control makes the poor and the mentally ill unhousable, because no one will build inexpensive housing when it is forced by law to be expensive. The sane and the already-rich get the rent-controlled apartments and the fancy townhouses in once-poor neighborhoods.

Regulation of electricity hurt householders by raising electricity costs, as did the ban on nuclear power. The Securities Exchange Commission did not help small investors. Federal deposit insurance made banks careless with depositors’ money. The conservation movement in the Western U. S. enriched ranchers who used federal lands for grazing and enriched lumber companies who used federal lands for clear cutting. American and other attempts at prohibiting trade in recreational drugs resulted in higher drug consumption and the destruction of inner cities and the incarcerations of millions of young men. Governments have outlawed needle exchanges and condom advertising, and denied the existence of AIDS.....

The case for free markets, and social freedom, is practical. It need not be ideological. It's based on the clear lessons of history. We all have the same stated goals. It's not about who cares more. It's about what works.

Admire McCloskey's post also for the writing. The author of "The Rhetoric of Economics" (Article and Book -- an absolute must-read for every young economist) knows what she's doing! Rather than write an article expanding on one of these points, or a three-volume encyclopedia explaining the factual basis of all of them, she make the withering case by stating each point just once, but layering all of them in one place.

Republicans Want To Own The Sullivan Ouster

The McDonnell forces, not content with a furious effort to control the upcoming board vote on Tuesday, to maintain the ouster of Sullivan, have now enticed the Wall Street Journal into one of the most astounding editorials in the paper's history. This editorial is so full of factual inaccuracies and outright distortions as to make you wonder about the facts cited in other editorials that the Journal runs. Read it in today's WSJ.

The conservative right is apparently vying to support Governor McDonnell's effort to claim credit for Sullivan's ouster. They are turning this into a right versus left controversy, even though the entire episode seemed to have been originally engineered by the left. But, maybe not. It is becoming increasingly clear that Governor McDonnell was in on this from the very beginning as the now-famous Darden email stated.

The McDonnell forces are pulling out all of the stops to control the vote to oust Sullivan and to keep the University in a state of turmoil for years to come. This will be the principal legacy of the McDonnell governorship. Far from his stated policy of "neutrality," the Governor and his team are doing everything in their power to remove Sullivan with finality. Such action will never, ever have the stamp of legitimacy.

As Gilmore did in years past, McDonnell is on a path to alienate his Republican base. Having worn out his welcome with Republicans, Gilmore found his political future in Virginia destroyed. His crushing defeat by Mark Warner was accomplished by a substantial number of Republicans voting for Democrat Warner. McDonnell is headed for the same future. He is systematically fighting the very people that elected him and he will find out, as Gilmore did, that his Republican base in Virginia is withering away.

It is not only the Board of Visitors that displays a remarkable lack of transparency. The Governor of Virginia should be honest and admit his role in the sacking of Sullivan. His team is fighting furiously, as I write this, to maintain her ouster. Why not be open about it instead of more hypocrisy?

Sunday, June 24, 2012

Legal News

Two legal items in last week's news caught my eye: The legal challenge to Dodd-Frank, and a challenge to Virginia's "certificates of need" for new hospitals. I've written about both from an economic, and slightly political-economy viewpoint. The legal challenges are a new and interesting angle.

Links:

"Certificates of need" for hospitals are one of the many barriers to entry enacted by state governments and enforced by state regulators. To start a hospital, a state board needs to give you one of these certificates, and all your competitors get to come to the hearing and complain that you're stealing their business. In Illinois, keeping up the profits of incumbents is written right there in the statute defining the board that hands out certificates.

Again, horrible economics, but governments have been using the fig-leaf of consumer protection to stifle competition and prop up politically-connected incumbents for centuries if not millenia.

Well, perhaps the framers of the constitution had more foresight than I thought. There is an interesting prospect that both of these horrible bits off economics are in fact unconstitutional and can be brought down by legal challenge.

Both threads will come together this week. We will hear on the constitutional challenge the law now called Obamacare even by its defenders. But here the legal challenge -- the mandate -- is one of the least objectionable pieces of economics. I wish stupid economics were unconstitutional, and lawyers could go after the heart of the bill. If the separation of powers case for Dodd-Frank works, perhaps they will, for the ill defined terms, arbitrary power, regulator discretion and so forth in the health law make even Dodd-Frank look good.

In the big picture, our Obamacare debate has focused on health insurance, but the awful economics and regulatory destruction of the health care markets should be higher on the list. Why can't you walk in to a hospital and have any idea what the real prices are? Why does "thank you, I'll pay cash" mean you'll get socked with a huge bill, not a nice discount? Anti-competitive regulation is a big answer. Perhaps the Virginia case can begin the dismantling of state and federal regulation strangling competition in health care.

----

The main legal challenge to Dodd-Frank centers on the Consumer Financial Protection Bureau. Gray and Purcell start with a nice quote from President Obama

Stupid, yes. But unconstitutional? Their argument rests on separation of powers, and "checks and balances:"

I wish the suit emphasized more the FSOC rather than the CFPB, which is a larger component of Dodd-Frank and a much bigger danger. But you don't have to be too much of a conspiracy theorist to realize why the big banks under the FSOC's thumb aren't willing to sign on to a complaint. It's rather courageous that so many small banks signed on. Given the CFPB's wide discretion, they are putting themselves at real risk.

Will it work? I don't know. The obvious counterargument is that this structure is set forth in legislation, passed by Congress and signed by the President. If they want to give up their power, they can do so. The complaint (p.29) already tries to counter this by pointing out precedents on the limitations of Congress' ability to devolve its power.

The complaint and oped get really mad about the director's appointment

Still, I do find the idea attractive (am I being too hopeful?) that something so awful in its economic structure is also unconstitutional -- and for much of the same reasons.

----

The Insitute for Justice summary of their complaint against Virgina's bureau is a nice primer on how state "consumer protection" is really "competitor protection,"

Well, you had me when you said hello, but why is this illegal, especially unconstitutional? Heck, taxi medallions work the same way. The IJ website says only

Yes, libertarians go to sleep each night praying that these interpretations will be reversed some day. But that is a different than hoping Dodd-Frank, Obamacare, Certificates of Need, and other ham-fisted economic policy can be declared unconstitutional on their own.

Not being a lawyer, I didn't track down the legal arguments on this one any further. I'll just leave the attempt as a ray of hope.

Links:

- Why Dodd-Frank is Unconstitutional, a WSJ OpEd by C. Boyden Gray and Jim Purcell, who are bringing the case.

- A nice video from WSJ in which Editor James Freeman explains the case;

- Press release, a list of links and details of the complaint from the Competitive Enterprise Institute

- The Insitute for Justice on "Colon Health Centers of America, LLC, et al. v. Hazel, et al." and their more extensive background

"Certificates of need" for hospitals are one of the many barriers to entry enacted by state governments and enforced by state regulators. To start a hospital, a state board needs to give you one of these certificates, and all your competitors get to come to the hearing and complain that you're stealing their business. In Illinois, keeping up the profits of incumbents is written right there in the statute defining the board that hands out certificates.

Again, horrible economics, but governments have been using the fig-leaf of consumer protection to stifle competition and prop up politically-connected incumbents for centuries if not millenia.

Well, perhaps the framers of the constitution had more foresight than I thought. There is an interesting prospect that both of these horrible bits off economics are in fact unconstitutional and can be brought down by legal challenge.

Both threads will come together this week. We will hear on the constitutional challenge the law now called Obamacare even by its defenders. But here the legal challenge -- the mandate -- is one of the least objectionable pieces of economics. I wish stupid economics were unconstitutional, and lawyers could go after the heart of the bill. If the separation of powers case for Dodd-Frank works, perhaps they will, for the ill defined terms, arbitrary power, regulator discretion and so forth in the health law make even Dodd-Frank look good.

In the big picture, our Obamacare debate has focused on health insurance, but the awful economics and regulatory destruction of the health care markets should be higher on the list. Why can't you walk in to a hospital and have any idea what the real prices are? Why does "thank you, I'll pay cash" mean you'll get socked with a huge bill, not a nice discount? Anti-competitive regulation is a big answer. Perhaps the Virginia case can begin the dismantling of state and federal regulation strangling competition in health care.

----

The main legal challenge to Dodd-Frank centers on the Consumer Financial Protection Bureau. Gray and Purcell start with a nice quote from President Obama

"Our financial system only works—our market is only free—when there are clear rules and basic safeguards that prevent abuse, that check excess, that ensure that it is more profitable to play by the rules than to game the system." We completely agree.As do I. "Rules." Which is not how Dodd-Frank is structured:

The FSOC can declare a financial firm "systemically important"—that is, too big to fail—based on "any" "risk-related factors" that it "deems appropriate." And the CFPB can punish even responsible lenders who in good faith offer loans that the bureau later deems to be "unfair," "deceptive" or "abusive."They echo my complaints about the FSOC.

Those open-ended standards place no limits on the regulators' power. Indeed, in January newly appointed CFPB Director Richard Cordray told Congress that he believes it is "probably not useful" to try to define in advance what an "abusive" lending practice is. Instead, he intends to use his enforcement powers to retroactively punish lenders based on his view of the "facts and circumstances" of each case.

Stupid, yes. But unconstitutional? Their argument rests on separation of powers, and "checks and balances:"

The Constitution empowers the president and Congress, as well as our courts, to prevent regulators from running amok with excessive, arbitrary or even partisan regulations.The details of the complaint adds lovely detail on the Alice-in-Wonderland quality of the words "abusive" "deceptive" and "unfair" practices, (see p. 10), adds the legal argument that theyare ex-post-facto constructs. Maybe the prohibition on bills of attainder can apply to regulatory decisions?

But Dodd-Frank does not honor checks and balances. It eliminates them. The CFPB is not subject to Congress's "power of the purse,"... Instead, Dodd-Frank lets the CFPB claim more than $400 million from the Federal Reserve each year and prohibits Congress from even reviewing that budget. The president's control over the CFPB is limited because by law he can remove the agency's director only under strictly limited circumstances. Finally, Dodd-Frank limits the courts' review of CFPB's legal interpretations.

I wish the suit emphasized more the FSOC rather than the CFPB, which is a larger component of Dodd-Frank and a much bigger danger. But you don't have to be too much of a conspiracy theorist to realize why the big banks under the FSOC's thumb aren't willing to sign on to a complaint. It's rather courageous that so many small banks signed on. Given the CFPB's wide discretion, they are putting themselves at real risk.

Will it work? I don't know. The obvious counterargument is that this structure is set forth in legislation, passed by Congress and signed by the President. If they want to give up their power, they can do so. The complaint (p.29) already tries to counter this by pointing out precedents on the limitations of Congress' ability to devolve its power.

The complaint and oped get really mad about the director's appointment

Moreover, Mr. Obama nullified one of Congress's few remaining limits on the CFPB—namely, Senate review and confirmation of its nominated director—by deeming the Senate to be in "recess" during a short break in early January and unconstitutionally appointing Mr. Cordray director without the Senate's advice and consentBut this point is really not about the structure of the bill, it is a criticism of President Obama's action. The statute says the director should be approved by the Senate. If the Administration acted unconstitutionally in its appointment of the director, I can see how they can reverse that action, but I don't see how that makes the statute unconstitutional. But it's better for me not to play lawyer.

Still, I do find the idea attractive (am I being too hopeful?) that something so awful in its economic structure is also unconstitutional -- and for much of the same reasons.

----

The Insitute for Justice summary of their complaint against Virgina's bureau is a nice primer on how state "consumer protection" is really "competitor protection,"

If you want to offer new healthcare services, even something as routine as opening a private clinic, you have to obtain special permission from the [Virginia] state government. And permission is not easy to come by: Would-be service providers have to persuade state officials that their new service is “necessary”—and they have to do so in a process that verges on full-blown litigation in which existing businesses (their would-be competitors) are allowed to oppose them. Not surprisingly, this process can be incredibly expensive, and it frequently results in new services being forbidden to operate at all.Both in Virginia and Illinois, these restrictions were also put in place in the name of "cost control," i.e. to stop businesses from "needlessly" building too much capacity. Our national policy is now going to echo these bright ideas.

To be clear, this requirement (called a certificate-of-need or CON program) has nothing to do with public health or safety. Separate state and federal laws govern who is allowed to practice medicine and what kind of medical procedures are or are not permitted. Virginia’s CON program only regulates whether someone is allowed to open a new office or purchase new equipment; it is explicitly designed to make sure new services are not allowed to take customers away from established healthcare services.

Well, you had me when you said hello, but why is this illegal, especially unconstitutional? Heck, taxi medallions work the same way. The IJ website says only

The Constitution protects individuals’ right to earn an honest living free from unreasonable government interference, and it prevents states from putting up unnecessary barriers to interstate commerce.Sorry guys, the constitution as currently interpreted doesn't say anything about a "right to earn an honest living." See the 1873 Slaughterhouse Case, (comments from George Will here) which found that "a citizen's 'privileges and immunities,' as protected by the Constitution's Fourteenth Amendment" do not extend to economic freedoms, so "a state may grant business monopolies to some of its citizens but not to others without running afoul of the Constitution." See Wickard v Filburn which found that the Federal Government can stop a farmer from growing wheat for his own use without permission. (Recently reinforced by Justice Scalia, in Gonzales v Raich.) And it's going to be hard to argue that opening a clinic or buying an MRI machine is protected interstate commerce.

Yes, libertarians go to sleep each night praying that these interpretations will be reversed some day. But that is a different than hoping Dodd-Frank, Obamacare, Certificates of Need, and other ham-fisted economic policy can be declared unconstitutional on their own.

Not being a lawyer, I didn't track down the legal arguments on this one any further. I'll just leave the attempt as a ray of hope.

A Reality Check from GASB

There are new rules coming out from the Government Accounting Standards Board (GASB) that will require public pension funds to recalculate their unfunded liability. The new rules still retain a "wishful thinking" component, but the new rules definitely move the calculations more toward reality and away from the current fantasy rules that public pension funds now use.

The bottom line issue is how to "value" the future payments that pension beneficiaries are expecting to receive. Current methods have absurdly low valuations on these future payments and, as a result, the employer contributions to these funds have always been absurdly inadequate. It has long been in the interest of politicians and board members to downplay the miserable funding status of these pension funds and to hope and pray that their inevitable blow-up will occur on someone else's watch.

Some states, Utah in particular, have dealt with these obligations in a straight forward fashion and enacted true reform of their public pension plans. Others, like Virginia, have enacted temporary band-aid solutions that mostly just obscure the true nature of the funding crisis.

Expect the usual knee-jerk response to the new GASB rules, which actually don't go far enough, from folks who fear that telling the truth about the true costs of these public pension plans would eviscerate the political support for the plans.

The bottom line issue is how to "value" the future payments that pension beneficiaries are expecting to receive. Current methods have absurdly low valuations on these future payments and, as a result, the employer contributions to these funds have always been absurdly inadequate. It has long been in the interest of politicians and board members to downplay the miserable funding status of these pension funds and to hope and pray that their inevitable blow-up will occur on someone else's watch.

Some states, Utah in particular, have dealt with these obligations in a straight forward fashion and enacted true reform of their public pension plans. Others, like Virginia, have enacted temporary band-aid solutions that mostly just obscure the true nature of the funding crisis.

Expect the usual knee-jerk response to the new GASB rules, which actually don't go far enough, from folks who fear that telling the truth about the true costs of these public pension plans would eviscerate the political support for the plans.

This is McDonnell's Decision

In a close vote on a state governing board, all eyes look to the Governor's mansion. If Sullivan is not reappointed, then it should be obvious to everyone what really happened here and who is responsible. Politicians change after they get elected. Their inner circle quickly descends to a small group of political hacks and the super rich. These folks usually have a very different agenda than the voters who elected the politicians and often are diametrically opposed to the views of the political party that the politician represents.

Members of governing boards, both governmental and corporate, usually have only one agenda -- to stay on the boards. Thus, they look to those who control reappointment in times of crisis. Not all, but most. Check the political contributions that board members make in the months leading up to a reappointment decision and you will find a clear pattern. This is human nature, not some evil conspiracy. That human nature is playing out now at the University of Virginia. Whether or not Sullivan is returned to the UVA presidency will come down to the votes of two or three key McDonnell allies. How they vote will tell all.

Members of governing boards, both governmental and corporate, usually have only one agenda -- to stay on the boards. Thus, they look to those who control reappointment in times of crisis. Not all, but most. Check the political contributions that board members make in the months leading up to a reappointment decision and you will find a clear pattern. This is human nature, not some evil conspiracy. That human nature is playing out now at the University of Virginia. Whether or not Sullivan is returned to the UVA presidency will come down to the votes of two or three key McDonnell allies. How they vote will tell all.

Saturday, June 23, 2012

Another Weekend Rambling.

Everywhere you look today there is a mention of how Chinese data is fake. Yawnnn! Have they discovered God in the laboratory? Of course almost everything that comes out of any Government is false. China may be faking 90% of what is reported but look closer at home. I think almost everything that USA reports are blatantly false. Be it BLS job data, GDP data, Housing data, Loan data or even serious things like WMD. Colin Powel even lied before the UN and US went to a false war on false pretext. So I fail to understand what the big deal about the false data out of China. Whoever believed it in the 1st place please raise your hand. You must believe in tooth fairy as well!

Europe has been the front and centre of our life for the last few months. But so it had been in these very months of 2010 and 2011. Every June, from 2010, we feel that Europe is coming to an end. The fact is, America will falter before Europe. If Europe is struggling because of its massive debt, if Japan is in depression because of its 200% + Debt:GDP ratio, just wait when the chickens come home to roost in USA. With its $100 Trillion unfunded liability, many more trillions of dollars of Muni Bonds, almost 100% official debt to GDP ratio, destruction is staring at the face of USA. Many of my American friends think that USA is the best house in the bad neighbourhood. Actually, it is the best camouflaged booby-trap in a jungle.

In a ZIRP environment, the only solution left to the Fed and politicians is to print more money. Already the money supply is running at 9% and yet we see deflation all around. The 10 year yield at the height of the economic crisis in 2008 was 2.10 % and now it is 1.67 %. So the bond market thinks that we are closer to a disaster now than we were at 2008. Every successive QE has demonstrated the law of diminishing return and just to get back to 1400 level of SPX, Bernanke will have to pump another trillion dollar. Even if he does that, nothing will change. And yet he will do it because his political master wants him to do so. The long term 30 year cycle of bond yield has topped now and in a matter of weeks and months, we will see yields rising. Time to scale in TBT.

The short term target remains as we discussed and nothing has changed. We might see a lower low on Monday before we shoot up one more time. If I think there is a trade worth taking, I will send the information through Twitter. The real damage will come after that which will force the hands of Bernanke. Barring one day, June 4th, there has been no panic in the market so far and just for this reason, I think selling is not over.

Those of you who swear by TA I have a nice article for you from Brian Shannon. Brian wrote a book on Technical Analysis:

The market is tricky, and it seems so even more lately. Technical analysis is often misinterpreted as an exact science, it is merely a tool which allows us to determine potential price based scenarios before we commit our money to a position.

Lately we have seen a lot of technical analysis misused. From a couple of closes below the 200 day moving average being interpreted as bearish, to a couple closes above the 50 day moving average being interpreted as bullish, or believing that one can buy the break above the “neckline” if the inverted head and shoulder pattern and then kick back and wait for the price objective to be met. These examples of ‘failed technical analysis’ are “proof” by doubters that technical analysis is useless. If you are going to succeed in the markets, risk management should be your first priority, regardless of what your timeframe is. I consider technical analysis to be the finest risk management tool that anyone can use if they really understand the psychology of the formation of patterns rather than focusing on pattern recognition alone.