Friday, February 26, 2010

Alphatrends weekly market wrap

Brian Shannon of Alphatrends takes us through his Weekly Wrap on Stocktwits TV with a technical look at the major US market averages and a view to the trading week ahead.

Brian's technical analysis videos tend to highlight the action of leading stocks and the major averages in multiple timeframes (hourly, daily, & weekly charts).

While I'm not as familiar with his trading style as others might be, I do like to check out his videos on a regular basis, in addition to following Brian's trading notes and market thoughts on Twitter.

Take a look at Shannon's market wrap, and if you like what you see, you can find additional episodes (and a variety of additional trading and investing themed content) at the Stocktwits TV archives.

Thursday, February 25, 2010

Altucher: Things I learned from Vic Niederhoffer

When James Altucher mentioned (on Twitter) that he was preparing an article about lessons learned while trading for Victor Niederhoffer, I knew that was one essay I'd be looking forward to.

Here's James on, "Ten Things I Learned While Trading for Victor Niederhoffer":

"I traded for Victor Niederhoffer for about a year starting in 2003. I was up slightly more than 100% for him, primarily trading futures using a quantitative approach. During that period I had one down month: June 2003.

Victor was a top trader for George Soros before starting his own fund in the ’90s and then writing the classic investment text “Education of a Speculator.” He then suffered one of several blowups in his career when his fund crashed to zero while on the wrong side of a couple of bets during the Asian currency crisis in 1997 (most notably, he was short S&P puts when the market crashed that year).

Despite that, Victor has consistently traded his own portfolio quite successfully and is one of the best traders I’ve seen in action. He still posts his daily comments on trading and the markets at his site dailyspeculations.com.

Here are 10 things I learned during my time trading for Victor: ..."

Read on as Altucher talks about the importance of testing your ideas, optimism, fearlessness, and protecting your downside (there's a lot more here too). Enjoy the essay and the lessons.

Here's James on, "Ten Things I Learned While Trading for Victor Niederhoffer":

"I traded for Victor Niederhoffer for about a year starting in 2003. I was up slightly more than 100% for him, primarily trading futures using a quantitative approach. During that period I had one down month: June 2003.

Victor was a top trader for George Soros before starting his own fund in the ’90s and then writing the classic investment text “Education of a Speculator.” He then suffered one of several blowups in his career when his fund crashed to zero while on the wrong side of a couple of bets during the Asian currency crisis in 1997 (most notably, he was short S&P puts when the market crashed that year).

Despite that, Victor has consistently traded his own portfolio quite successfully and is one of the best traders I’ve seen in action. He still posts his daily comments on trading and the markets at his site dailyspeculations.com.

Here are 10 things I learned during my time trading for Victor: ..."

Read on as Altucher talks about the importance of testing your ideas, optimism, fearlessness, and protecting your downside (there's a lot more here too). Enjoy the essay and the lessons.

Tuesday, February 23, 2010

Richard Russell: Last Man Standing

Even though I'm able to read Richard Russell's Dow Theory Letters at the town library (they are subscribers), it's nice to find snippets from his daily remarks up on 321gold. It's convenient, and I can easily share samples of his excellent writing with others.

Here's one that I'd like to share with you, a recent update from Russell on gold and the state of America's finances called, "Last Man Standing".

"A final thought. One could stay in US dollars and gold. If the dollar goes to hell, rising gold could make up for the loss in purchasing power.

A hundred years ago gold and silver were the only items accepted as money. Paper money was carried around because it was convenient as opposed to gold and silver, which are heavy. Besides, if you had any doubt about your paper, you could turn it in at any national bank for gold, "the dollar was as good as gold." Furthermore, the dollar was backed by one of the strongest and most prosperous nations on earth.

Today the dollar is backed only by "the full faith and credit of the United States," the greatest debtor the world has ever seen. Questions are now arising about the credit-worthiness of sovereign debt. Many analysts believe that the US will never, ever, be able to pay off its debt, which is now not only rising but is compounding.

It's obvious that the Obama administration is putting off the solution of our debt and deficit problems to other future administrations. This is always a dangerous procedure.

It's the reason why our children and grandchildren will not inherit the fun and easy life that we live. I've talked about sacrifice before -- our children will be making some of the sacrifices that my own generation made (and I hope one of the sacrifices won't be war)...

Read on to understand why "Americans have forgotten the meaning of gold and silver", and check out more of Russell's remarks at the 321gold archive and at his website (linked above).

You'll see why he's one of the most fascinating writers around (on almost any subject), and you will definitely get some perspective from a guy who's been around and seen more than most.

Here's one that I'd like to share with you, a recent update from Russell on gold and the state of America's finances called, "Last Man Standing".

"A final thought. One could stay in US dollars and gold. If the dollar goes to hell, rising gold could make up for the loss in purchasing power.

A hundred years ago gold and silver were the only items accepted as money. Paper money was carried around because it was convenient as opposed to gold and silver, which are heavy. Besides, if you had any doubt about your paper, you could turn it in at any national bank for gold, "the dollar was as good as gold." Furthermore, the dollar was backed by one of the strongest and most prosperous nations on earth.

Today the dollar is backed only by "the full faith and credit of the United States," the greatest debtor the world has ever seen. Questions are now arising about the credit-worthiness of sovereign debt. Many analysts believe that the US will never, ever, be able to pay off its debt, which is now not only rising but is compounding.

It's obvious that the Obama administration is putting off the solution of our debt and deficit problems to other future administrations. This is always a dangerous procedure.

It's the reason why our children and grandchildren will not inherit the fun and easy life that we live. I've talked about sacrifice before -- our children will be making some of the sacrifices that my own generation made (and I hope one of the sacrifices won't be war)...

Read on to understand why "Americans have forgotten the meaning of gold and silver", and check out more of Russell's remarks at the 321gold archive and at his website (linked above).

You'll see why he's one of the most fascinating writers around (on almost any subject), and you will definitely get some perspective from a guy who's been around and seen more than most.

Sunday, February 21, 2010

John Allison on "Leadership and Values"

John A. Allison, then acting CEO and Chairman of BB&T bank (now retired), gives a talk on "Leadership and Values" at the University of Virginia's Darden School of Business.

Why am I linking to this lecture by John Allison? Very simply, Allison's excellent talk addresses a greatly overlooked theme in American business and life today: establishing one's code of personal ethics.

Now what makes John Allison qualified to deliver such a lecture?

Allison, who we highlighted (and who the NY Times profiled) in our post, "BB&T prefer liberty and reason to bailouts", grew the North Carolina-based BB&T bank by leaps and bounds while it gained plaudits from customers and the business community for its integrity and high rates of customer satisfaction.

While large banks and mortgage lenders across the country sank their customers, themselves, and our overall economy through their overexposure to residential housing and subprime mortgage loans, Allison and BB&T remained focused on ethical capitalism and engaging in "win-win" transactions that benefited the bank as well as its customers.

In his talks on "Leadership and Values", Allison, an admirer of Ayn Rand's philosophy of Objectivism, discusses the importance of integrity, examining your ethical framework, egalitarianism and moral relativism vs. objective truth, and the road to self- improvement.

We'll let John Allison do the talking now. Check out the video above, or see this more recent clip of a very similar talk at Marshall University with a Q&A session from students and community members. Enjoy the discussion!

Friday, February 19, 2010

Market Wrap: Chris Puplava & Co.

Guys, if you're taking a long view of the markets and studying up on economic trends this weekend, you might want to take a look at Chris Puplava's latest market wrap for FSO.

Chris has put together an update on the credit markets, with some thoughts on US Treasuries and the direction of long-term interest rates.

There's also quite a bit of data and commentary on China's holdings of US govt. debt and the "state of the states" - US state finances. Plus, you'll get a look at the economic recovery, bank lending practices, market sentiment indicators, and more. Lots to look at here.

And if you've got time to check out Martin Goldberg's recent market wrap on the Emerging Markets (and ETF $EEM in particular), you'll find some worthwhile technical commentary there as well.

Have a good weekend, and if you're surfing our part of the blogosphere, check back in for some new updates & video posts. See you then.

Chris has put together an update on the credit markets, with some thoughts on US Treasuries and the direction of long-term interest rates.

There's also quite a bit of data and commentary on China's holdings of US govt. debt and the "state of the states" - US state finances. Plus, you'll get a look at the economic recovery, bank lending practices, market sentiment indicators, and more. Lots to look at here.

And if you've got time to check out Martin Goldberg's recent market wrap on the Emerging Markets (and ETF $EEM in particular), you'll find some worthwhile technical commentary there as well.

Have a good weekend, and if you're surfing our part of the blogosphere, check back in for some new updates & video posts. See you then.

Wednesday, February 17, 2010

To short or not to short?

I'm reading some of the great stuff put out by the bloggers in the Stocktwits network and I wanted to share two great posts, from Joe Fahmy and Keith McCullough, on the pros and cons of short-selling.

I'm reading some of the great stuff put out by the bloggers in the Stocktwits network and I wanted to share two great posts, from Joe Fahmy and Keith McCullough, on the pros and cons of short-selling.The first post, by Joe Fahmy, is entitled, "Why I Hate Shorting Stocks". Here's an excerpt from Joe's lead in:

"When I called for a market correction in mid-January, I received several emails asking me why I don’t recommend short ideas. In my Introduction blog post, I talk about finding an investment philosophy that fits your personality…and quite simply, shorting is not for me.

The title of this article is not meant to offend anyone, as I never try to impose my trading style on anyone. I actually believe that shorting is a necessary part of the stock market and that short-covering can add stability to a correcting or “free-falling” market. Nevertheless, it doesn’t fit my personality and here are my reasons why: ..."

Joe is one of the most interesting and educational stock traders/bloggers I've followed on Stocktwits and Twitter. In this post, he has taken the time to lay out why, in his personal view, short-selling is not conducive to his personality and trading style.

As I noted in the comments section of his post, I think that even traders with considerable short-selling experience might benefit from his arguments. It's all about what works for you.

On the flipside, we have a post from Keith McCullough at the Hedgeye Blog which argues short-selling is a necessary component of risk management:

"If you want to be a warrior of risk management, you need to be able to survive the daily battles of short selling. This is not a blood sport, nor is it one that deserves the attention of your emotions. It’s a mathematical martial art that requires flexibility and laser-like focus.

Overall, I’m probably a better short seller and risk manager than I am long term investor. That’s probably because I have more experience in down markets than I have in up ones. I entered this daily battle of ‘don’t lose money’ at a hedge fund in the year 2000. The first 3 years of my ‘be right or be gone’ experience were in down markets. Call me biased, but the only business I trust owning for the long term is the one I am building with my own hands..."

There you have it. Two differing views on a long-debated subject of relevance for investors and speculators, each from professional traders sharing their thoughts on Twitter and their respective blogs. Hope you enjoy their thought-provoking posts!

Sunday, February 14, 2010

Video: Russia Forum 2010

Must watch video of a panel discussion with Marc Faber, Hugh Hendry, Nassim Taleb, Michael Power, and others at The Russia Forum 2010.

As moderator, Marc Faber begins the discussion by asking the panel members how they would invest $100 million for the year ahead. A varied discussion on the global economy, geopolitics, inflation vs. deflation, risk, food and energy systems, and the rise of emerging markets ensues.

Great macro discussion with seeds of investing ideas and global macro trades sprinkled throughout. Don't miss this one, and thanks to Jay at Marketfolly for highlighting this discussion.

Friday, February 12, 2010

How far will Greece's problems spread?

So just to follow up on our last post about debt problems in Greece and the EU, I'm hearing that some people are having a hard time making sense of this crisis and what it means for the whole of Europe.

To that end, I've decided to highlight a few helpful articles that will further our understanding of these sovereign risk issues.

We're seeing a growing worry that problems in Greece, UK, Spain, et. al, will spread throughout the eurozone and signal problems for other developed nations as well. Are these fears justified? Let's take a quick look and see what we find.

First off, The Economist reported yesterday that the EU summit on Greece yielded only "vague promises of solidarity" and no concrete plans for how a bailout of Greece by larger EU nations might come about.

Here's an opening excerpt from that piece:

"“PRETTY catastrophic”. That was the verdict of a depressed-looking diplomat, at the end of a Brussels summit on Thursday February 11th that saw European Union leaders issue a ringing, but alarmingly vague, pledge of “determined and co-ordinated action” to preserve the euro zone from the risk of a Greek sovereign default.

To that end, I've decided to highlight a few helpful articles that will further our understanding of these sovereign risk issues.

We're seeing a growing worry that problems in Greece, UK, Spain, et. al, will spread throughout the eurozone and signal problems for other developed nations as well. Are these fears justified? Let's take a quick look and see what we find.

First off, The Economist reported yesterday that the EU summit on Greece yielded only "vague promises of solidarity" and no concrete plans for how a bailout of Greece by larger EU nations might come about.

Here's an opening excerpt from that piece:

"“PRETTY catastrophic”. That was the verdict of a depressed-looking diplomat, at the end of a Brussels summit on Thursday February 11th that saw European Union leaders issue a ringing, but alarmingly vague, pledge of “determined and co-ordinated action” to preserve the euro zone from the risk of a Greek sovereign default.

The vagueness of the bail-out promise was no mystery. After years of footing the bills for successive Euro-crises, Germany is in a truculent mood. Of the 16 countries that share the single currency, most came to Brussels ready to spell out, in some detail, how they might come to the aid of Greece, without breaching “no bail-out” rules that prevent the EU from assuming the debts of countries in the euro zone."

Would a bailout of Greece accomplish much? According to SocGen strategist, Albert Edwards, it would only serve to delay what he sees as the inevitable: a Eurozone breakup.

Meanwhile, Niall Ferguson writes in a recent FT piece that the "Greek crisis is coming to America". He argues, as we (and others) have, that the US seems to be taking false comfort in its temporary "safe haven" status, when in fact it should be looking at the longer-term effects of its own debt explosion.

"For the world’s biggest economy, the US, the day of reckoning still seems reassuringly remote. The worse things get in the eurozone, the more the US dollar rallies as nervous investors park their cash in the “safe haven” of American government debt. This effect may persist for some months, just as the dollar and Treasuries rallied in the depths of the banking panic in late 2008.

Yet even a casual look at the fiscal position of the federal government (not to mention the states) makes a nonsense of the phrase “safe haven”. US government debt is a safe haven the way Pearl Harbor was a safe haven in 1941..."

So I think we have enough here to highlight the risks that investors and economic thinkers are currently mulling over. The question remains: will fiscal problems in places like Greece, Spain, and Dubai spread to established financial institutions and larger economies?Wednesday, February 10, 2010

Understanding Greece and the EU

As I understand it, a bailout of any EU member nation (say Greece) is illegal under the Euro-establishing Maastricht treaty.

However, Josh Lipton at Minyanville points out a possible loophole should the European nations want to skirt that rule:

"The only real question for members of the Eurozone, says Dr. Ed Yardeni of Yardeni Research, is whether to boot out or bail out the Greeks...

...The economist emphasizes that the Maastricht rules contains a "no bailout" clause to ensure that a member country's budgetary problems couldn’t spill over and damage the credit rating of the Eurozone as a whole.

However, he writes in a recent research note, there's belief that the Eurozone could get around this by invoking Article 122 of the Lisbon Treaty, which allows the European Union to throw a financial life-preserver to a member country suffering tough times."

So the next question for market watchers and EU citizens (or their political elites) to consider is whether or not the larger European nations should structure a bailout for Greece and other fiscally weak member states.

Actually, it's a question that's been tossed around for months as Mark Crosby notes in, "EU bailout no solution to Greece's problems". Take a look at this article to get an easily digestible overview of the problems facing Greece and the eurozone.

However, Josh Lipton at Minyanville points out a possible loophole should the European nations want to skirt that rule:

"The only real question for members of the Eurozone, says Dr. Ed Yardeni of Yardeni Research, is whether to boot out or bail out the Greeks...

...The economist emphasizes that the Maastricht rules contains a "no bailout" clause to ensure that a member country's budgetary problems couldn’t spill over and damage the credit rating of the Eurozone as a whole.

However, he writes in a recent research note, there's belief that the Eurozone could get around this by invoking Article 122 of the Lisbon Treaty, which allows the European Union to throw a financial life-preserver to a member country suffering tough times."

So the next question for market watchers and EU citizens (or their political elites) to consider is whether or not the larger European nations should structure a bailout for Greece and other fiscally weak member states.

Actually, it's a question that's been tossed around for months as Mark Crosby notes in, "EU bailout no solution to Greece's problems". Take a look at this article to get an easily digestible overview of the problems facing Greece and the eurozone.

Monday, February 8, 2010

Bloomberg: weak dollar, inflation "illusory"

Apparently, the continued erosion of the US dollar's purchasing power and the ensuing inflation we've witnessed since 1975 has been merely an illusion.

So says Bloomberg in an astonishingly misleading article entitled, "Weak dollar illusory as correlated trade gains show":

"For all the concern over the $1.6 trillion U.S. budget deficit and record debt load, the dollar is as valuable now as 35 years ago. Measured against a basket of currencies from the Group of 10 nations proportioned by how they trade against each other, the greenback is up about 3 percent since 1975, according to Bloomberg Correlation-Weighted Currency Indexes.

That was four years after the Bretton Woods agreement, set up in 1944 to link currencies to the price of gold, collapsed. The U.K. pound has dropped 34 percent and the Canadian dollar has fallen 6 percent."

Using the Bloomberg Correlation-Weighted Currency Index as a value benchmark, the writer purports to show that the dollar is just "as valuable" now (more so!) as it was in the period just after Nixon "closed the gold window" and removed the last vestiges of the gold standard in 1971.

Here's an explanation of Bloomberg's weighted currency index:

"The Bloomberg Correlation-Weighted Currency Indices (BCWI) provide an indication of the relative strength or weakness of one currency against the world, i.e., a representative basket of currencies."

The problem, of course, with assigning the dollar (or any fiat currency) a value based on the measure of a basket of currencies is that these currencies are all going down (gradually, over time) together. There is no consistent reference point for measuring true value.

This is how one editorialist, named Goldrunner, explained it:

"...We introduced how the Dollar Index can only be considered a fiat pricing scheme since it cannot reflect the value of the Dollar. Value can only be determined against a constant reference point- certainly not against a basket of items that are constantly changing."

This is particularly true during a time period when most currencies are being devalued like the time period we are now entering. This is because a group of currencies that are all falling in value, if priced against each other, will leave the currency falling the least looking as if it has risen. Down is then up."

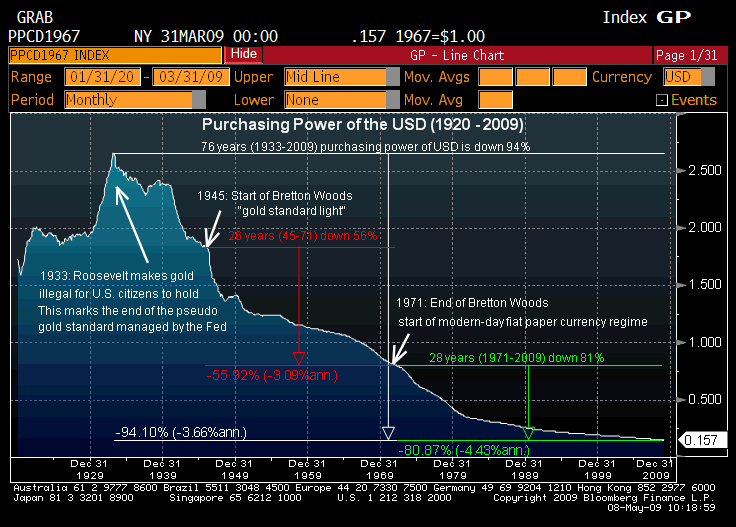

You may be interested to see how the US dollar has fared against gold in recent years.

So says Bloomberg in an astonishingly misleading article entitled, "Weak dollar illusory as correlated trade gains show":

"For all the concern over the $1.6 trillion U.S. budget deficit and record debt load, the dollar is as valuable now as 35 years ago. Measured against a basket of currencies from the Group of 10 nations proportioned by how they trade against each other, the greenback is up about 3 percent since 1975, according to Bloomberg Correlation-Weighted Currency Indexes.

That was four years after the Bretton Woods agreement, set up in 1944 to link currencies to the price of gold, collapsed. The U.K. pound has dropped 34 percent and the Canadian dollar has fallen 6 percent."

Using the Bloomberg Correlation-Weighted Currency Index as a value benchmark, the writer purports to show that the dollar is just "as valuable" now (more so!) as it was in the period just after Nixon "closed the gold window" and removed the last vestiges of the gold standard in 1971.

Here's an explanation of Bloomberg's weighted currency index:

"The Bloomberg Correlation-Weighted Currency Indices (BCWI) provide an indication of the relative strength or weakness of one currency against the world, i.e., a representative basket of currencies."

The problem, of course, with assigning the dollar (or any fiat currency) a value based on the measure of a basket of currencies is that these currencies are all going down (gradually, over time) together. There is no consistent reference point for measuring true value.

This is how one editorialist, named Goldrunner, explained it:

"...We introduced how the Dollar Index can only be considered a fiat pricing scheme since it cannot reflect the value of the Dollar. Value can only be determined against a constant reference point- certainly not against a basket of items that are constantly changing."

This is particularly true during a time period when most currencies are being devalued like the time period we are now entering. This is because a group of currencies that are all falling in value, if priced against each other, will leave the currency falling the least looking as if it has risen. Down is then up."

You may be interested to see how the US dollar has fared against gold in recent years.

Chart courtesy of Bloomberg.com

While the index measurement shows the dollar to be holding steady (thanks to the "down is up" bias of said index) in the chart above, gold has still handily outperformed over a five year period. In fact, the precious metal, which started the period at a price of $411 an ounce has increased to over $1050 an ounce, a gain of over 150 percent.

Gold has increased over that period, not (as some would have you believe) because of a speculative "bubble", but because it's role as an international safe haven currency and a historical store of value (purchasing power) have been rediscovered by a new generation of investors.

There is far more to today's Bloomberg article than the dollar/gold relationship and confusion over the loss of our currency's purchasing power over time (see, for example Tim Geithner's eminently fadable opinion on the US government's AAA debt rating), but we'll have to address some of these themes in our next post (Update: see, "How far will Greece's problems spread?" for more on this).

In short, I've come to expect a bit more from Bloomberg than this. Hopefully, next time they will do their readers a real service by reporting the truth about our currency's gradual decline in purchasing power, sad as it may be. They might even look to their own data service & charts for help.{kind=link}

Thursday, February 4, 2010

Jim Chanos: "overheating" in China

Here's what I'm currently watching: noted short-seller and hedge fund manager, Jim Chanos gives a talk on "Overheating & Overindulgence" in China at the London School of Economics Alternative Investments Conference (see also: Bloomberg video).

We've noted here before that Chanos is hugely bearish on the Chinese economy and looking to bet against its overheated real estate and construction businesses by shorting commodities and ancillary suppliers.

In this presentation Chanos offers his thoughts on China's GDP growth, its credit excesses, and the interplay of its economic and political system. Very interesting stuff, even if Jim Rogers is skeptical over the recent findings of newly-minted China experts.

Is he right? Given my limited knowledge of the situation, I'm inclined to agree with Marc Faber (a friend of both Chanos and Rogers) who notes that Jim Chanos is "hyper smart" and willing to back his thesis, though it's uncertain how the timing of a Chinese bust will play out.

Related articles and posts:

1. Pivot Capital Report: China's Investment Boom - Finance Trends.

2. Is China Headed Towards Collapse? - Politico.

3. Marc Faber: China bubble bad for commodities - Tech Ticker.

Wednesday, February 3, 2010

Does real GDP growth signal recovery?

Over on Twitter this morning, The Kirk Report tweeted a link to a Wells Capital Management report that offers some upbeat news on prospects for economic recovery.

Here's an excerpt from that report entitled, "Current Real GDP Recovery Looks as Strong as 1975, 1982 Recoveries":

"Despite a strong fourth-quarter real GDP report, the debate surrounding the strength of the contemporary economic recovery lingers. Most seem to anticipate a subpar recovery similar to the last two during the early 1990s and after the dot-com meltdown in the early 2000s.

However, although the current recovery is only two quarters old, it is thus far closely tracking the strong recoveries of 1975 and 1982..."

There follows some interesting charts and data summaries which lead the authors to conclude that the current recovery, measured on real GDP growth, is much stronger than many had believed it would be.

I am happy to consider positive arguments for economic growth, but I'm also left to wonder how reliable these real GDP figures are, given the way we measure inflation statistics these days.

Tim Iacono at TMGM has a nice little chart that illustrates this relationship between real economic growth and inflation. Note how drastically the real GDP figures can change when inflation is overstated or understated.

For a more thorough discussion of why GDP figures are an unreliable and "heavily politicized" data point, please see this post on John Williams' Shadow Stats report on 4th quarter GDP.

Added notes: this blog post from the Daily Kos site offers an upbeat outlook on the GDP numbers and jobs recovery, similar to the Wells Capital report. What are your thoughts?

Here's an excerpt from that report entitled, "Current Real GDP Recovery Looks as Strong as 1975, 1982 Recoveries":

"Despite a strong fourth-quarter real GDP report, the debate surrounding the strength of the contemporary economic recovery lingers. Most seem to anticipate a subpar recovery similar to the last two during the early 1990s and after the dot-com meltdown in the early 2000s.

However, although the current recovery is only two quarters old, it is thus far closely tracking the strong recoveries of 1975 and 1982..."

There follows some interesting charts and data summaries which lead the authors to conclude that the current recovery, measured on real GDP growth, is much stronger than many had believed it would be.

I am happy to consider positive arguments for economic growth, but I'm also left to wonder how reliable these real GDP figures are, given the way we measure inflation statistics these days.

Tim Iacono at TMGM has a nice little chart that illustrates this relationship between real economic growth and inflation. Note how drastically the real GDP figures can change when inflation is overstated or understated.

For a more thorough discussion of why GDP figures are an unreliable and "heavily politicized" data point, please see this post on John Williams' Shadow Stats report on 4th quarter GDP.

Added notes: this blog post from the Daily Kos site offers an upbeat outlook on the GDP numbers and jobs recovery, similar to the Wells Capital report. What are your thoughts?

Monday, February 1, 2010

SIGTARP report: housing bubble 2.0?

Last night, FT came out with this report on Sig-TARP probing possible insider trading at US banks:

"Neil Barofsky, the special inspector-general overseeing the US government’s financial rescue efforts, is to probe allegations of insider trading among bank executives and their associates.

"Neil Barofsky, the special inspector-general overseeing the US government’s financial rescue efforts, is to probe allegations of insider trading among bank executives and their associates.

Eight of the largest banks in the US received between $2bn and $25bn in October 2008 under a programme to prop up the financial system led by Hank Paulson, then Treasury secretary.

Dozens more institutions followed and Mr Barofsky, who examines the troubled asset relief programme, is looking into whether information improperly made its way to trading rooms during a feverish period in which the government and banks were frequently exchanging information..."

The article goes on to say that much of the latest SIG-TARP report focuses on government's increased role in the housing market.

"Much of Sig-Tarp’s new report is given over to an examination of the housing market and the multitude of government schemes designed to support lending and help homeowners avoid foreclosure.

“The government has done more than simply support the mortgage market,” the report said. “In many ways it has become the mortgage market with the taxpayer shouldering the risk that had once been borne by the private investor.”

Mr Barofsky added: “All of the things that were broken in the housing market and the different roles that different private players have played, some of what we recognise now . . . actually contributed to the bubble and to the ensuing crisis are really being replicated by government actors.”"

The myriad government bank lending programs have become too numerous and confusing for me. I imagine that it's very easy to lose track of all this information unless you are a writer, blogger, or news junkie particularly focused on the bank bailouts and lending programs designed to prop up US housing prices.

To catch up with some of these details, we might want to turn to Dr. Housing Bubble's blog for their new post on the "Stunning STIGTARP report" and "The Subtle Nationalization of the Banks and Housing Market". I can see some interesting data and insights leafing through this post, and will now give it a careful read.

Subscribe to:

Posts (Atom)