Jesse Jackson Jr, a Congressman from Illinois, has a new idea to kill off some more jobs. He wants to raise the minimum wage from its current level, $ 7.25, to $ 10. As if unemployment, especially among youth, isn't high enough!

Remember what a $ 10 minimum wage law says. It says that it is against the law to hire anyone that you intend to pay less than $ 10 per hour. It outlaws a transaction between employer and potential employee. Basically, it makes criminals out of employers who offer jobs. So, why offer jobs anyway?

Jackson, of course, is among America's wealthiest individuals, which is typical of people that propose things like this that cut the legs out from under the poorest amongst us. What does he care if another million or so join the ranks of the unemployed? Might give him another voter or two.

If you want more apples, make it against the law to buy one for less than $ 10 apiece. That should do a lot for the consumption of apples! That's the Jesse Jackson Jr way to increased apple production.

Thursday, June 7, 2012

Wednesday, June 6, 2012

Francois Hollande is Deluded

Like Scott Walker, Francois Hollande is delivering on his promises...unfortunately. His first real proposal is to lower the retirement age for social security back to 60 from 62, reversing the move, instituted by Sarcozy, from 60 to 62. This is really not as big a deal as it looks, since no one under the age of 50 will receive any benefits anyway, whether they retire at 60 or 62.

But, it does reveal the clear direction of Hollande's thinking. Like many French politicians who preceded him, he thinks France is rich and can afford to fund more than half of its population in a life of leisure. It turns out he's wrong, like many French politicians who preceded him, but if he can just fool enough people before he leaves office then I think he'll be happy.

France has been trying to slide into total decadence and chaos for several generations. Only the strength of the world economy has kept this sick puppy afloat. But, the world economy isn't likely to oblige this time around and it is probably over for France. So why not cut the retirement age. Why not take it to 55? If you're going to go bust anyway, what real difference does it make where you set the retirement age. Make it zero and cut to the chase. There are no funds set aside for it anyway and the shrinking work force can't possibly pay for it. So, why not go for it.

Hollande, of course, has found the magic elixir -- tax rich people -- the Obama theme song. But even if you confiscated all the wealth of every single French family with more than $ 1 million in assets, you still could not come close to funding their social security system, even if you left the age at 62. So really. What difference does it make whether the retirement age is 60 or 62. Not much.

Watch Greece carefully. Greece is everyone's future.

But, it does reveal the clear direction of Hollande's thinking. Like many French politicians who preceded him, he thinks France is rich and can afford to fund more than half of its population in a life of leisure. It turns out he's wrong, like many French politicians who preceded him, but if he can just fool enough people before he leaves office then I think he'll be happy.

France has been trying to slide into total decadence and chaos for several generations. Only the strength of the world economy has kept this sick puppy afloat. But, the world economy isn't likely to oblige this time around and it is probably over for France. So why not cut the retirement age. Why not take it to 55? If you're going to go bust anyway, what real difference does it make where you set the retirement age. Make it zero and cut to the chase. There are no funds set aside for it anyway and the shrinking work force can't possibly pay for it. So, why not go for it.

Hollande, of course, has found the magic elixir -- tax rich people -- the Obama theme song. But even if you confiscated all the wealth of every single French family with more than $ 1 million in assets, you still could not come close to funding their social security system, even if you left the age at 62. So really. What difference does it make whether the retirement age is 60 or 62. Not much.

Watch Greece carefully. Greece is everyone's future.

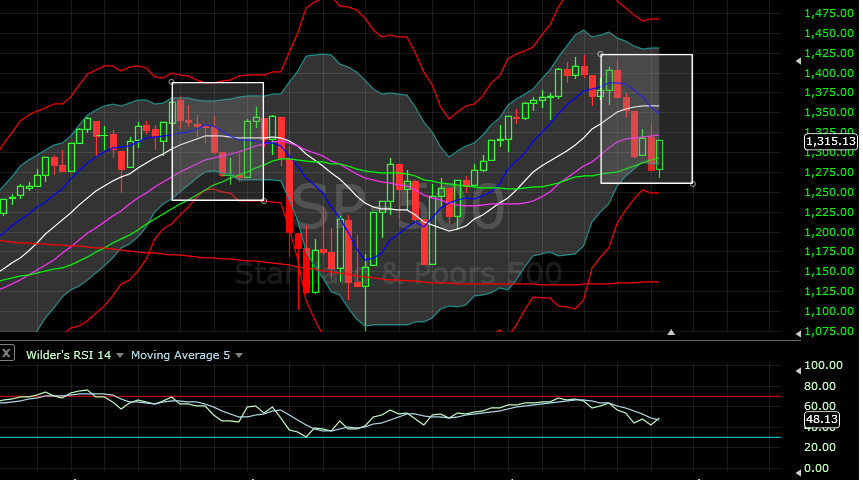

Rip The Face Off Rally.

That was some monster rally! It was special in many ways. This was the biggest SPX rally since 12/20, biggest VIX Drop since 5/21 and biggest 10 year yield jump since 3/14. But we are not surprised because we knew it would come. I have been writing about it since: gosh, I even forget myself. This is the reason I did not short the market even when SPX broke 1284. I am afraid I keep repeating myself so very often that you might find it un-exciting. But on the other hand, I have called most of the major turns and bounces correctly without being dramatic. Now that the rally is here, what do we do with it? That depends what is your goal. Are you able to follow the futures overnight and be ready to pounce on the keyboard of your computer the moment the market opens? Do you consider yourself a nimble trader? If so, then you are ready to play. But if you have a regular job with kids and family, you have to go to office in the morning and do hundred other things besides being glued to the computer, you might give it a pass. For those regular folks, cash is king.

There is nothing fundamental in this rally. I have been showing this chart from the age of Adam.

This is a weekly chart. So let us see where it reaches by the end of the week.

What I am sure off is that we will test the lows but I am not sure whether we will have new lows. Like the Elliot wave guys, I have two possible counts. The preferred count is that we go up this week or early part of next week and selling resumes from June 20 when Bernanke extends Operation Twist and does not come up with real free money. The alternate count is, this being a presidential election year cycle, we deviate from earlier script and keep going up if Bernanke starts QE 3 on June 20.

(Actual not updated)

For now though I will stick with my preferred count.

In the morning before the market opened I sent out Tweets that I plan to go long on Nasdaq, Crude and Gold. If you have joined me in Twitter you would have got the actionable twitter even before the market opened (8.30 AM Eastern) and you would have been ready to take part in this spectacular rally. The model portfolio has been updated with the positions. But I am not really happy with Gold and I might dump it in a day or two depending on its price action. It is signaling that there will not be any QE on June 20th. Euro on the other hand declared that the world is not going to end just yet. I know it is a false hope but if that gives the bounce, I will take it.

Let us see how the market digest this rally and what is in store tomorrow. I would be happy with 1330 and surprised if we reach 1360, although that has been my range. But market is the boss. We just want to be in the good books and on the right side of boss.

Thanks for reading http://bbfinance.blogspot.com/. Please forward / re-tweet / post it on your wall and join me in twitter to get those actionable tweets. (Twitter @ BBFinanceblog)(Stocktwits: Worldoffinance)

The Sun Shines in Wisconsin

A state known for its "progressive" politics rejected union bullying yesterday and, by re-electing Governor Scott Walker, cast a vote for fiscal sanity. Even in Wisconsin, government finances are still in serious peril. What Walker has done so far represents only a baby step toward getting Wisconsin's state financial house in order. They still have massive unfunded pension liabilities, both at the state level and at the local level. The size of these unfunded liabilities are several orders of magnitude worse than the $ 3.6 billion budget gap that Walker has closed in the last two years. But, still. It is a beginning and brings a glimmer of sunshine to a state that was careening off into disaster until Walker came along.

As in Europe, the situation in the various states in America is simply a question of numbers. This is not about politics. There is no political solution for Europe or for the American states. There is no set of circumstances that will enable them to pay their debts. So, it is time to acknowledge that their debts are unpayable. Once you do that, then there are solutions. But, there are no viable solutions if politicians continue to pretend that their are some grand solutions for the current problems. There are none.

Wisconsin will, sooner or later, have to change their retirement and health care deals for public employees. There is no set of taxes or rates of economic growth that will fund their current projected obligations. That is the same problem that is faced by California, Illinois, New York, New Jersey and, yes, even in Virginia. The sooner these liabilities are restructured, the less will be the pain for all.

As in Europe, the situation in the various states in America is simply a question of numbers. This is not about politics. There is no political solution for Europe or for the American states. There is no set of circumstances that will enable them to pay their debts. So, it is time to acknowledge that their debts are unpayable. Once you do that, then there are solutions. But, there are no viable solutions if politicians continue to pretend that their are some grand solutions for the current problems. There are none.

Wisconsin will, sooner or later, have to change their retirement and health care deals for public employees. There is no set of taxes or rates of economic growth that will fund their current projected obligations. That is the same problem that is faced by California, Illinois, New York, New Jersey and, yes, even in Virginia. The sooner these liabilities are restructured, the less will be the pain for all.

Tuesday, June 5, 2012

I almost agree with Summers

Larry Summers has an interesting pair of Opeds in the Washington Post and on Reuters. By picking and choosing just a bit, I can find a lot to agree with -- and I can point to the central factual question separating his view and mine.

Interestingly, Larry sides with those of us who think monetary policy is close to ineffective at this moment, and thus neither the problem nor the source of even symptomatic relief.

Where we differ, of course, is on whether the government should simply restructure the existing debt to long maturities, or whether it should use these low rates to go on a borrow and spend binge. Larry:

The question is, Are there indeed sizeable positive real return projects that our government can, and will, invest in, and realize positive returns?

Let's be clear, what counts here to "improve their future fiscal position": Can the government by borrowing spending $1 now reap more than $1 of tax revenue or realize more than $1 of spending reduction in the future? By spending $1 more now can and will the deficit really decline by more than $1 in the future, in such a clear and transparent way that bond markets see it and believe it? For this exercise, you don't get to count social benefits, external effects, stimulus and so on -- the acid test is simple: $1 more deficit now, results in more than $1 less deficit later.

And "sizeable" is important too. We are running more than $1 trillion dollars of deficits, and these are set to explode. To "improve our fiscal position" in a noticeable way, we need to cut that deficit by say $100 billion dollars. So, suppose the government can finance at zero percent real rates, and suppose that it can find projects with 5% real rate of return -- an optimistic assumption, especially risk adjusted. Still, to make a $100 billion dent in a $1 trillion deficit, that means the government needs to find $2 trillion of investment projects which give a risk free 5% return!

Where are these investment projects?

I note most of our government's "investment" projects consist of high speed rail, altenrative energy boondoggles, photovolatics that need protection from Chinese imports and so on. Say what you will about side benefits, but none of these projects has a remote chance of returning a positive return to the US Treasury. The Wall Street Journal recently reviewed health and human services "investment portfolio" to savage effect. If the Treasury gets a cent back on these it will be a miracle. As Larry himself found out when running the stimulus program, shovel-ready projects are hard to find, even if you do not want a positive rate of return to the Treasury but simply want to get money out the door.

So what does Larry have in mind as concrete positive return investments?

Well, that's nice. But first of all, does any of this really produce $1 more deficit today and $1 less deficit in the future? If we do a bunch of maintenance now, does that mean we cut budgets in the future? Or will that simply mean "great, we don't have to pay for maintenance, we can use this year's budget to do new things?"

But even with that warning in mind, is there really two trillion dollars of maintenance and building leases that can be moved forward? Or is this a drop in the bucket of our budget problems?

That's the real weakness. Larry Summers, who knows the Federal Budget far better than I, writing opeds on positive return government investments, can't come up with more than accelerating maintenance and buying some leased space. How much is that? Is it even $10 billion, not the $2 trillion needed to make a difference in the budget?

That's the disagreement, make your own judgements. It's easy to think of all sorts of nice-sounding projects -- which Larry curiously doesn't mention. Roads, bridges, education, etc. Perhaps Larry has too much experience with roads and bridges to nowhere, education money down ratholes and so forth; spending that has some use, but does not produce $1.05 of new tax revenue for every $1 spent.

OK, I also question a bit analysis like this:

Interestingly, Larry sides with those of us who think monetary policy is close to ineffective at this moment, and thus neither the problem nor the source of even symptomatic relief.

... one has to wonder how much investment businesses are unwilling to undertake at extraordinarily low interest rates that they would be willing to undertake with rates reduced by yet another 25 or 50 basis points. It is also worth querying the quality of projects that businesses judge unprofitable at a -60 basis point real interest rate but choose to undertake at a still more negative real interest rate. There is also the question of whether extremely low safe real interest rates promote bubbles of various kinds.Most importantly, Larry thinks this is a golden moment to lengthen the maturity of government debt

Any rational chief financial officer in the private sector would see this as a moment to extend debt maturities and lock in low rates – exactly the opposite of what central banks are doing. In the U.S. Treasury, for example, discussions of debt-management policy have had exactly this emphasis. But the Treasury does not alone control the maturity of debt when the central bank is active in all debt markets.

...Any rational business leader would use a moment like this to term out its debt. Governments in the industrialized world should do so too.I've been screaming this from the rooftops for a few years now. "Lock in low rates" puts it mildly. When markets start to question whether the US will ever address our budget problems, it will be spectacularly better if we have locked in long maturity debt, and are not trying to roll over short term debt. Then long term interest rates can rise, bondholders take a hit, but we don't have a Greek, Spanish or Italian crisis on our hands. It's good insurance, and remarkably cheap at the current moment. The Treasury is trying, weakly. The Fed is offsetting all these efforts by buying up long term debt and selling short term debt.

Where we differ, of course, is on whether the government should simply restructure the existing debt to long maturities, or whether it should use these low rates to go on a borrow and spend binge. Larry:

... governments that enjoy such low borrowing costs can improve their creditworthiness by borrowing more, not less, and investing in improving their future fiscal position even assuming no positive demand stimulus effects of a kind likely to materialize with negative real rates.There is a rational argument on both sides: It is correct as a matter of economic theory that if the government can borrow at slightly negative real rates, and invest in projects with positive rates of return, then the government's overall fiscal position is better.

The question is, Are there indeed sizeable positive real return projects that our government can, and will, invest in, and realize positive returns?

Let's be clear, what counts here to "improve their future fiscal position": Can the government by borrowing spending $1 now reap more than $1 of tax revenue or realize more than $1 of spending reduction in the future? By spending $1 more now can and will the deficit really decline by more than $1 in the future, in such a clear and transparent way that bond markets see it and believe it? For this exercise, you don't get to count social benefits, external effects, stimulus and so on -- the acid test is simple: $1 more deficit now, results in more than $1 less deficit later.

And "sizeable" is important too. We are running more than $1 trillion dollars of deficits, and these are set to explode. To "improve our fiscal position" in a noticeable way, we need to cut that deficit by say $100 billion dollars. So, suppose the government can finance at zero percent real rates, and suppose that it can find projects with 5% real rate of return -- an optimistic assumption, especially risk adjusted. Still, to make a $100 billion dent in a $1 trillion deficit, that means the government needs to find $2 trillion of investment projects which give a risk free 5% return!

Where are these investment projects?

I note most of our government's "investment" projects consist of high speed rail, altenrative energy boondoggles, photovolatics that need protection from Chinese imports and so on. Say what you will about side benefits, but none of these projects has a remote chance of returning a positive return to the US Treasury. The Wall Street Journal recently reviewed health and human services "investment portfolio" to savage effect. If the Treasury gets a cent back on these it will be a miracle. As Larry himself found out when running the stimulus program, shovel-ready projects are hard to find, even if you do not want a positive rate of return to the Treasury but simply want to get money out the door.

So what does Larry have in mind as concrete positive return investments?

They should accelerate any necessary maintenance projects..

..accelerating replacement cycles for military supplies. Similarly, government decisions to issue debt, and then buy space that is currently being leased, will improve the government’s financial position as long as the interest rate on debt is less than the ratio of rents to building values..

Well, that's nice. But first of all, does any of this really produce $1 more deficit today and $1 less deficit in the future? If we do a bunch of maintenance now, does that mean we cut budgets in the future? Or will that simply mean "great, we don't have to pay for maintenance, we can use this year's budget to do new things?"

But even with that warning in mind, is there really two trillion dollars of maintenance and building leases that can be moved forward? Or is this a drop in the bucket of our budget problems?

That's the real weakness. Larry Summers, who knows the Federal Budget far better than I, writing opeds on positive return government investments, can't come up with more than accelerating maintenance and buying some leased space. How much is that? Is it even $10 billion, not the $2 trillion needed to make a difference in the budget?

That's the disagreement, make your own judgements. It's easy to think of all sorts of nice-sounding projects -- which Larry curiously doesn't mention. Roads, bridges, education, etc. Perhaps Larry has too much experience with roads and bridges to nowhere, education money down ratholes and so forth; spending that has some use, but does not produce $1.05 of new tax revenue for every $1 spent.

OK, I also question a bit analysis like this:

It is more likely that negative feedback loops are again taking over as falling incomes lead to falling confidence, which leads to reduced spending and yet further declines in income.This particular "negative [sic] feedback loop" is, to put it politely, a mechanism new to economic theory. Maybe it works. But I prefer policy involving trillions of my dollars to be based on well-worked out theories with some basis in rigorous theoretical and empirical analysis, not just the latest interesting story.

Sometimes There Is No Trade.

1284 has been taken back but barely just. The market seems to be moving along the script written and depending on what action Draghi takes tomorrow, it might aim for the stars. How far it will go up is anybody’s guess. We better keep in mind that it is a counter trend rally and expecting the market to go up when the trend is down is again an expensive proposition. Unless you are nimble trader, do not even bother with the bounce and wait for the correction to get over. If you must, you may even think of shorting it when a sizable bounce has been achieved. Then again, you must know what you are doing.

I read a lot of fellow bloggers, traders, rational thinkers as well as irrational nuts. In my life time, I have followed many Pandits only to find that nobody knows any better. Sometimes however we come across words said or written which are profound and strike a chord right away. The following is an example of such. It came from Josh Brown of The Reformed Broker:

· It is okay to admit when you don't have an edge.

· It is okay to say that you simply have no idea what's happening next.

· It is okay to sit out the possibility of an oversold bounce or a big snapback rally.

· It is okay to shut down the trading software and shut your mouth.

· There are forces at work here that many do not respect. There is "unprecedented" and then there is this, whatever the hell this turns out to be.

· You have a trading plan for bank runs? For the spontaneous dissolution of the world's largest economy? Congratulations on that, you're the only one.

· I understand that sentiment is so bad that literally any positive news will mean a sharp spike in the markets. But so what?

· And what happens after? Why does anyone think that this spike will be sustainable in the absence of actual improvement on the China/Europe/US employment front? Why would anyone other than the most nimble traders be worried about missing it?

· And also, it can always get worse.

· Respect the fact that we have no idea how far this can go before it has "gone too far". Respect the fact that once again, there is no leadership, no Man Behind the Curtain and that even the best and brightest and most connected and well-read are themselves grasping at straws here.

· There is no solution, only a choice of what may be the least bad. There is no consensus, no one alive has ever seen anything like this.

· I opt not to try to be cute here. I opt to look and listen and bide my time.

· Sometimes there simply is no trade. I believe this is one of those times.

I have printed it out and now it is right before my eyes where I can see it all the time and remind myself to have proper discipline. The 1st rule of the game: do not lose money. The 2ndrule: Read rule # 1.

Among all the bounces in all sectors, Crude will possibly give the best opportunity for a short term trade. Because it is so oversold. I will decide tomorrow whether to take a trade in Crude. But only when it is safe.

There is nothing much to say today. Everyone is tired of bad news. The funny thing is, none of the news coming out of Europe is new and they were there even in 2011. I remember last year I wrote about the pink elephant in the room that is Italy followed by Spain. Nobody seems to remember Italy yet but believe me it will come. But I think the biggest danger to the world capitalism will come from USA. USA has already started to monetize debt through back door and in six months time, they will be forced to do it openly. Bernanke will fight the scare of deflation with more money printing and when the bubble burst, USA will have massive inflation. It seem to be far away but it will arrive one fine day.

For now, we just wait and plan how best to save our capital. Thanks for reading http://bbfinance.blogspot.com/. Please forward / re-tweet / post it on your wall and invite others to join. (Twitter @ BBFinanceblog)(Stocktwits: Worldoffinance)

"More Europe, Not Less"

So says Angela Merkel. The idea is that if only Europe will "centralize" fiscal decision making and commercial bank regulation," then Germany may be willing to participate in a Europeanization of member country debt. There are only two problems with this solution: 1) centralizing fiscal decision making makes no difference at all; 2) commercial bank regulation has never been known to prevent financial crises and bank failures. All this shows is that Merkel doesn't understand what the problem is. No politician seems to get it.

The problem is simple: the welfare state has undermined the fiscal health of the Eurozone. There are two reasons, both stemming the from the same principle: when you promise people that they can receive income and services without paying for them, then two things happen: 1) people quit working and saving to provide for themselves; 2) you have to borrow unlimited amounts of money to fund the promises that you have made to people since they no longer have any plans to provide for themselves.

No amount of "centralization" of fiscal decision making can possibly matter. This is an imaginary fig leaf designed to make sure that the ultimate collapse in Europe occurs after Merkel leaves office. It does nothing to prevent that collapse.

"Not on my watch" seems to be the only theme of European and US policy. No one seriously wants to tackle the fundamental problem. If you don't dismantle the welfare state, it will dismantle itself in a chaotic, dehumanizing way. We can see this taking place in Greece and Spain today. This same dismantling process will be visiting Illinois and California in the near future.

Contrary to the views of the Krugmans and Stiglitz's of the world, there are no simple answers that can turn "no revenues" into "revenues." Someone, somewhere, must foot the bill. Who is that to be? If I am not willing to pay for my old age and my medical care and my education, etc., then who pays? Bondholders?

Centralizing decision making and increasing regulation will have no effect on the European financial crisis, since it does not address the problems in the Eurozone. It simply provides politicians, like Merkel, cover while they prepare for their own comfortable retirement.

The problem is simple: the welfare state has undermined the fiscal health of the Eurozone. There are two reasons, both stemming the from the same principle: when you promise people that they can receive income and services without paying for them, then two things happen: 1) people quit working and saving to provide for themselves; 2) you have to borrow unlimited amounts of money to fund the promises that you have made to people since they no longer have any plans to provide for themselves.

No amount of "centralization" of fiscal decision making can possibly matter. This is an imaginary fig leaf designed to make sure that the ultimate collapse in Europe occurs after Merkel leaves office. It does nothing to prevent that collapse.

"Not on my watch" seems to be the only theme of European and US policy. No one seriously wants to tackle the fundamental problem. If you don't dismantle the welfare state, it will dismantle itself in a chaotic, dehumanizing way. We can see this taking place in Greece and Spain today. This same dismantling process will be visiting Illinois and California in the near future.

Contrary to the views of the Krugmans and Stiglitz's of the world, there are no simple answers that can turn "no revenues" into "revenues." Someone, somewhere, must foot the bill. Who is that to be? If I am not willing to pay for my old age and my medical care and my education, etc., then who pays? Bondholders?

Centralizing decision making and increasing regulation will have no effect on the European financial crisis, since it does not address the problems in the Eurozone. It simply provides politicians, like Merkel, cover while they prepare for their own comfortable retirement.

Subscribe to:

Posts (Atom)