The University of Virginia Board of Visitors laid down the gauntlet by naming McIntire Business School Dean Zeithaml as the "interim President." It is hard to see this appointment as anything but a thumb in the eye to the University faculty and student body, concerned that outside financial interests have taken over University governance. There was no vote taken on the resignation and/or termination of President Teresa Sullivan, avoiding the hard question of who does or does not support her removal, not to mention the haunting question of why. As has become normal operating procedure for this Board of Visitors, all relevant activity took place in secret under the cloak of "executive sessions," further arousing the suspicions of those who view all of this as a massive conspiracy.

This sets the stage for a protracted battle between virtually the entire University of Virginia community and the school's governing Board and raises serious questions about where future funding will come from, given recent statements from major donors. The idea that this will "soon blow over" is wishful thinking. The road ahead probably signals the decline of what once was one of the very top public universities in the country. Nothing good lies ahead as the cohesion required for a major institution to thrive has been ripped asunder.

Surprisingly, Governor McDonnell has decided to go with this outcome and he now earns the dubious distinction of being the Governor who, effectively by proxy, removed the first woman President in the history of the University of Virginia. I guess he wanted this mantle, otherwise he might have acted differently. I suspect he must know by now that Mitt Romney has no interest in adding him to his presidential run this year. Ironically, this entire episode could easily be enough of a political problem for Republicans to ensure an Obama victory in Virginia in this year's presidential election, even though Sullivan's removal seems to have been mainly orchestrated by two Board members first appointed by Democratic governors.

Tuesday, June 19, 2012

Monday, June 18, 2012

Patents and copyright? "Great artists steal"

Came across this clip of Apple CEO, Tim Cook complaining that the ongoing tech patent wars are a "pain in the ass".

Granted, this is a topic that's recently been covered by Mark Cuban, or going farther back, by Bastiat in his "Three Stages of Invention".

However, one could look beyond Tim Cook's complaints to examine the very idea of the supposed necessity of patents and copyrights. The book, Against Intellectual Monopoly does just that, arguing: "Patents and copyrights do not promote economic progress but impede it."

Note this passage, from the same book, which calls attention to the fact that patents can block the market's progress by preventing product imitation, development, and refinement:

Without Matisse, would we know Picasso? Steve Jobs quoting Picasso: "good artists copy, great artists steal."

Granted, this is a topic that's recently been covered by Mark Cuban, or going farther back, by Bastiat in his "Three Stages of Invention".

However, one could look beyond Tim Cook's complaints to examine the very idea of the supposed necessity of patents and copyrights. The book, Against Intellectual Monopoly does just that, arguing: "Patents and copyrights do not promote economic progress but impede it."

Note this passage, from the same book, which calls attention to the fact that patents can block the market's progress by preventing product imitation, development, and refinement:

"Imitation is a great thing. It is among the most powerful technologies humans have ever developed … imitation is a technology that allows us to increase productive capacity. Innovators increase productive capacity directly...".

Without Matisse, would we know Picasso? Steve Jobs quoting Picasso: "good artists copy, great artists steal."

The Great Game.

I quote from Mark Grant:

“It is the Great Game. They try to lure you into their various traps; I try to keep you out. They offer headlines from countless sources and I try to tell you what things really mean. They make use of a giant propaganda machine and I chant alone in the wilderness. They make up stories and present them as accurate data and I try to give you the facts. They want your money and I want you to “Preserve your Capital.” They are as diabolical in their pursuits as Professor Moriarty was in his. They are the political masterminds and I am a sort of Sherlock Holmes trying to analyze and conclude one case after the other. You may listen or you may not but I pay for my own supper while others ask for their compensation first. It is their Game, my Game; it is the Great Game”.

“Has all my instruction been for naught? You still read the official statement and believe it. It's a game, dear man, a shadowy game. We're playing cat and mouse; cloak and dagger.”

-Sherlock Holmes, A Game of Shadows

I could not have said it any better.

Bottom line, “ Cash”, at least till FOMC is over and we see the market reaction. I am very certain that the bearded one will not come up with candies for the market on June 20th but who knows. At least I am not taking any bet on the outcome and am content to sit it out.

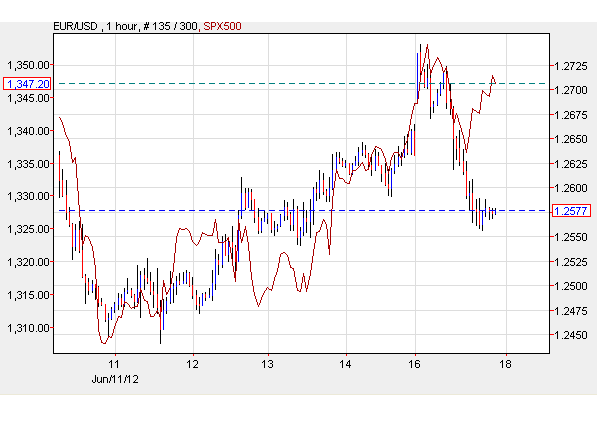

Just like last Sunday, Euro spiked up and faded thereafter. But precious metal sector did not rally. Even when Equities held up for the day, credits was down and bonds were up. A correlation between SPX and Euro shows that the sync broke today.

Normally in such situations, either one catches up. Because of the market sentiment with Euro, I think in the very short term, there are less chances of Euro going up. Logically therefore, SPX will catch it downward but it may remain elevated till Wednesday. Question is how much down SPX will go from here? And therein lays the answer for week after. If SPX can hold 1300-1320 level this week, the next move would be higher. But that will be a bull trap, not a real up-move. More so if it comes without QE. If you are confused, just remember that we will have chop fest for the next two weeks but the selling is not over.

My take therefore is the same as last weekend. Nothing has been fixed. Market cannot go up without additional liquidity. Till that comes, the risk is to the downside in intermediate time frame although in short time frame, we may see higher highs. A heaven sent opportunity for the day traders but for a normal investor it is the worst kind of nightmare possible.

Thanks for reading http://bbfinance.blogspot.com/ . Please forward / re-tweet / post it on your wall and join me in twitter. (Twitter @ BBFinanceblog)(Stocktwits: Worldoffinance)

Bloomberg TV link

I did a Bloomberg TV interview this morning on Euro debt crisis. I can't seem to insert the video here, so you'll have to follow the link if you're curious.

Update: I figured out how to embed bloomberg vidoes!

Update: I figured out how to embed bloomberg vidoes!

UVA Board Facing a Tidal Wave

They should have seen this coming. Major large donors are now abandoning the UVA Board in its effort to defend its decision to sack President Terry Sullivan. The current Provost John Simon added his voice of protest to that of former President John Casteen over the board's yet-to-be-explained removal of Sullivan. More than 800 faculty, staff and onlookers convened quietly in the Darden School auditorium last night to watch the Faculty Senate endorse a resolution expressing "no confidence" in the University's Board. UVA's Student Honor Council weighed in with its own letter expressing views that can't be encouraging for the Board.

Who's left?

Within the next 24 hours, I would expect some major changes in board composition as well as some change of course by the Board itself in the Sullivan ouster episode. The Board simply does not have the horses at this point and it is time to sound the retreat. Having the authority to fire Sullivan is just not enough. There needs to be some buy-in somewhere for this action and, thus far, there isn't any. Look for some kind of capitulation today by the UVA Board. Only the Governor and his staff seem content with the current situation and that will change too when they finally wake up and smell the coffee.

Who's left?

Within the next 24 hours, I would expect some major changes in board composition as well as some change of course by the Board itself in the Sullivan ouster episode. The Board simply does not have the horses at this point and it is time to sound the retreat. Having the authority to fire Sullivan is just not enough. There needs to be some buy-in somewhere for this action and, thus far, there isn't any. Look for some kind of capitulation today by the UVA Board. Only the Governor and his staff seem content with the current situation and that will change too when they finally wake up and smell the coffee.

Sunday, June 17, 2012

A glimmer of hope?

Weekend Update.

On Monday the Greeks decide whether to vote for the Easter Bunny or Santa Claus to solve their fiscal problems. What is Europe planning to do next?

Sunday's New York Times had an unusually cogent article on European events over the weekend, reporting on events with thoughtful analysis:

For years the mantra has been, stimulus and crisis management today, and "structural reform program" to be implemented in the vague far off future. They've figured out it won't work. Decades of previous good times did not bring structural reform.

But..

---

What about the immediate problem, the bank run, no longer "imminent" but gaining steam every day?

A cross-national deposit insurance scheme, while banks are already stuffed with sovereign debt, is back to Plan A, run for the exit and stiff Germany with the bill. Which "automatically encounters opposition in Germany."

A Supreme Bank Regulator to stop banks from gorging on sovereign debt in the first place might have been good idea, perhaps. (The concept "sovereign debt is risky" isn't necessarily beyond the ability of national regulators to comprehend, even with Basel rules denying it.) But it's way too late for that now.

Bottom line: Waffling again. No serious plan to stop the bank run already in place. You can't stop the crisis by saying you'll invent a totally new regulation regime to keep the banks from taking risks.

----

What about looming sovereign defaults?

The one big lesson to learn from this debacle is that deficit limit rules do not avoid sovereign defaults. A currency union without fiscal union needs to allow sovereign default.

As far as quelling the panic, good luck that "we really mean the deficit targets this time" will have any effect.

---

What are they going to do now, to stop the unraveling that is likely to happen in weeks?

---

Bottom line. Mr. Draghi is saying the right words on growth. But these plans to address bank runs and sovereign defaults are not realistic. And the pace of events is quickening. The time to actually implement a pro-growth policy, and stop financial panic by convincing markets it will really happen, is getting shorter and shorter.

On Monday the Greeks decide whether to vote for the Easter Bunny or Santa Claus to solve their fiscal problems. What is Europe planning to do next?

Sunday's New York Times had an unusually cogent article on European events over the weekend, reporting on events with thoughtful analysis:

The head of the European Central Bank and other euro zone leaders worked on Saturday on a grand vision... the plan will push for countries to remove the regulations and layers of bureaucracy that inhibit competition, keep young people out of the work force or make it difficult to start a new business....Halelujah! Growth -- the classical, growth-theory, higher productivity, bend-up-the-trendline, long-run kind of growth, not the quick espresso stimulus kind of growth (if that even works) -- is the only hope for Europe to repay debt rather than face the awful choices of default or inflation. At least we understand this is the central answer and without it, all the rescue plans will fail.

Over the years, countries have repeatedly pledged to clear the rules that hinder competition and led to chronically anemic growth. If the euro zone grew faster, tax receipts would rise and the debts of countries like Spain or Italy would seem less daunting

For years the mantra has been, stimulus and crisis management today, and "structural reform program" to be implemented in the vague far off future. They've figured out it won't work. Decades of previous good times did not bring structural reform.

“There is a long-standing agenda on growth,” Mr. Draghi told a gathering of economists on Friday in Frankfurt. “It is time to implement it.”---

But..

But it is unclear whether yet more pledges of reform, which would face significant hurdles, will calm financial markets.Correct. Quite a challenge, I'd say. How do you establish a "binding timetable?"

The euro zone has no shortage of plans and pacts intended to end years of sluggish growth and impose discipline on its 17 members.

The challenge for Mr. Draghi and the plan’s authors....will be to package their plan in a way that makes investors believe something will get done.

The most difficult task for Mr. Draghi and the other leaders may be to establish a binding timetable, to ensure that political leaders do not drag their feet.

The leaders are “only capable of acting at gunpoint” — when markets force them to, Willem H. Buiter, chief economist at Citigroup, said...But once markets "force them to" act, by a huge bank run, refusing to buy government debt, running from the currency, it will be too late for a structural reform plan to have any chance.

---

What about the immediate problem, the bank run, no longer "imminent" but gaining steam every day?

Under the plan, euro zone leaders will seek to establish the central bank as supreme bank regulator with broad powers, in place of the relatively toothless European Banking Authority.Catch 22. We've got a bank run. How to stop it? Ah, deposit insurance! But who is going to pay for that? "Countries" are not credible. The whole problem is that "countries" used their banks as piggy banks, stuffing them with sovereign debt. So, if the countries default on their sovereign debt, the banks go under, and the same "countries" obviously don't have the money to guarantee deposits.

Countries would also create a deposit insurance program to augment national programs. The goal would be to reassure ordinary depositors and prevent bank runs, an imminent danger in Spain as well as Greece. But any sharing of financial burdens almost automatically encounters opposition in Germany.

A cross-national deposit insurance scheme, while banks are already stuffed with sovereign debt, is back to Plan A, run for the exit and stiff Germany with the bill. Which "automatically encounters opposition in Germany."

A Supreme Bank Regulator to stop banks from gorging on sovereign debt in the first place might have been good idea, perhaps. (The concept "sovereign debt is risky" isn't necessarily beyond the ability of national regulators to comprehend, even with Basel rules denying it.) But it's way too late for that now.

Bottom line: Waffling again. No serious plan to stop the bank run already in place. You can't stop the crisis by saying you'll invent a totally new regulation regime to keep the banks from taking risks.

----

What about looming sovereign defaults?

For now, the most important new tool is a half-dozen rules known as the Six-Pack, which took effect in December. In coming months, the European Commission will be able to impose fines on euro zone countries of up to 0.2 percent of their gross domestic products if they flout rules on public debts and deficits.Oh yeah, right. The same Spanish government you just lent 100 billion euros to pour down the rathole of its banks, that one. You're going to tell them to pay you a fine of 0.2 pct of GDP because they're borrowing too much money..from you?

The one big lesson to learn from this debacle is that deficit limit rules do not avoid sovereign defaults. A currency union without fiscal union needs to allow sovereign default.

As far as quelling the panic, good luck that "we really mean the deficit targets this time" will have any effect.

---

What are they going to do now, to stop the unraveling that is likely to happen in weeks?

Mario Draghi, the president of the central bank and one of the authors of the plan, said Friday that it would be unveiled within days, ahead of a meeting of European leaders at the end of June.Well, that's good. I hope there still is a euro at the end of June.

---

Bottom line. Mr. Draghi is saying the right words on growth. But these plans to address bank runs and sovereign defaults are not realistic. And the pace of events is quickening. The time to actually implement a pro-growth policy, and stop financial panic by convincing markets it will really happen, is getting shorter and shorter.

Greek Vote: What Happens Next.

It transpired exactly as I thought. Greeks elected pro-bailout parties because they want other Europeans to pay for their debt. They elected the same political parties who are responsible for this mess in the 1st place but I suppose they have no alternative. The Fox is in charge of the hen house. What happens next?

FT Alphaville has this informative piece:

http://ftalphaville.ft.com/blog/2012/06/17/1047971/greece-the-post-election-questions/

And what about the pop in Euro? Oh that? It is already climbing down. Folks will soon realise that there will not be any Central Bank money pumping come Monday and Ben is going to disappoint as well on June 20.Nothing will come out of G20 as well. It could not have been any worse for the bulls in the short term. Things did not change and the bad news is not bad enough.

Lets see where it ends by next week.

I am happily sitting out of the whole drama.

Subscribe to:

Posts (Atom)